Founded in August 1994, HDFC Limited (“HDFC” or “Bank” or “Company”) is engaged in commercial banking activities in India. The Bank classifies its business in four segments:

1) Treasury; Corporate

2) Wholesale Banking

3) Retail Banking; and

4) Other Banking Operations

Apart from accepting deposits and providing loans, HDFC also provides life, health, and general insurance products under its subsidiary HDFC ERGO; mutual funds, asset management under its listed subsidiary HDFC AMC and online trading facility. HDFC earns non-fee based income from various other service offerings including national pension system, bank guarantee, bill discounting, merchant banking, cash management, depository, E-Commerce, trade finance, ATM, Internet and mobile banking, telephone banking, payment, fund transfer, electronic clearing, safe deposit locker, cash deposit machine, and online tax payment services.

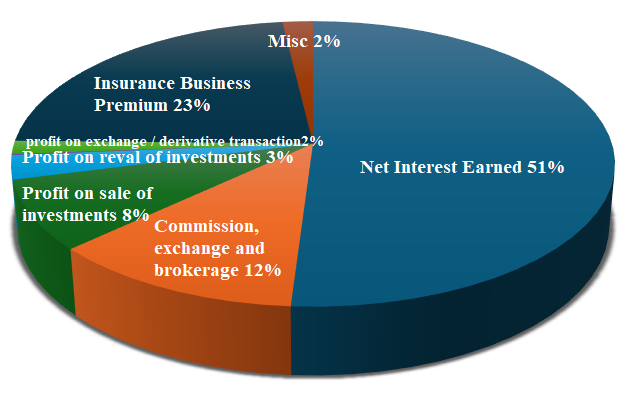

Here’s a look at how HDFC Bank makes its money.

| PARTICULARS | Rs in Cr |

| Interest Earned | 283649 |

| Interest Expended | 154138 |

| Net Interest Earned | 129511 |

| Commission, exchange and brokerage | 30621 |

| Profit on sale of investments | 20095 |

| profit on revaluation of investments | 6957 |

| profit on sale of building | 199 |

| profit on exchange / derivative transaction | 3870 |

| Insurance business premium income | 57858 |

| Miscellaneous income | 4742 |

| Total | 253853 |

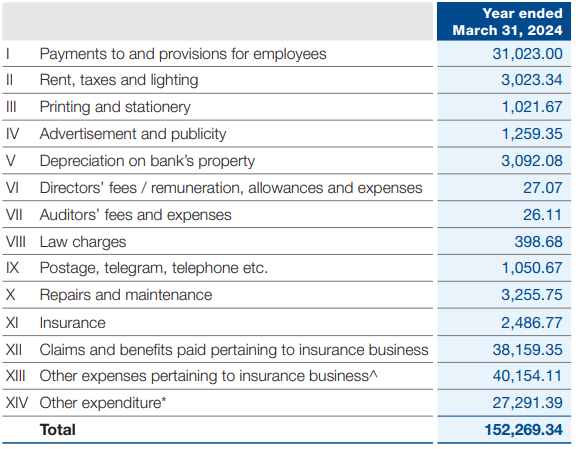

Note on HDFC BANK’s Expenditure

In terms of expenses, the above chart only accounts for interest expenses. In addition to interest paid out below table shows where HDFC spends its revenue.

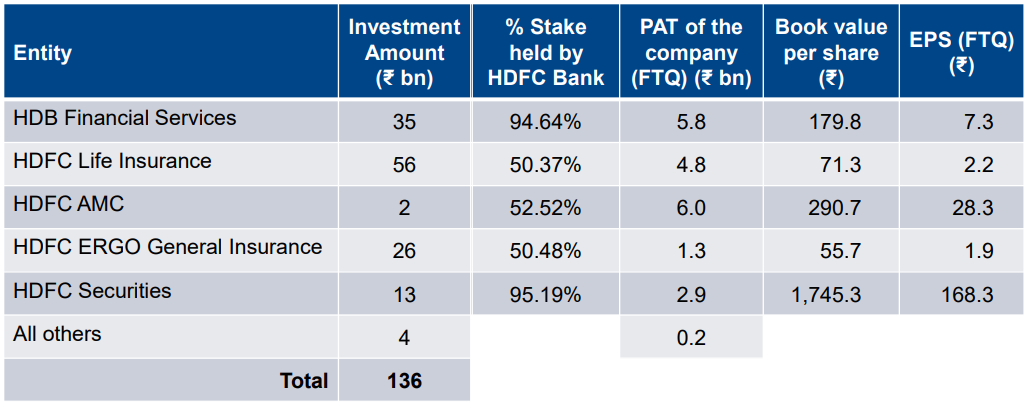

HDFC Subsidiaries as of 30 June 2024

In addition to its 8,851 branches, HDFC Bank’s subsidiaries have their own network of branches and employees. Below is a snapshot of HDFC’s interest in its subsidiaries.

WHAT’S GOING FOR THE HDFC BANK – WHAT’S CHANGED

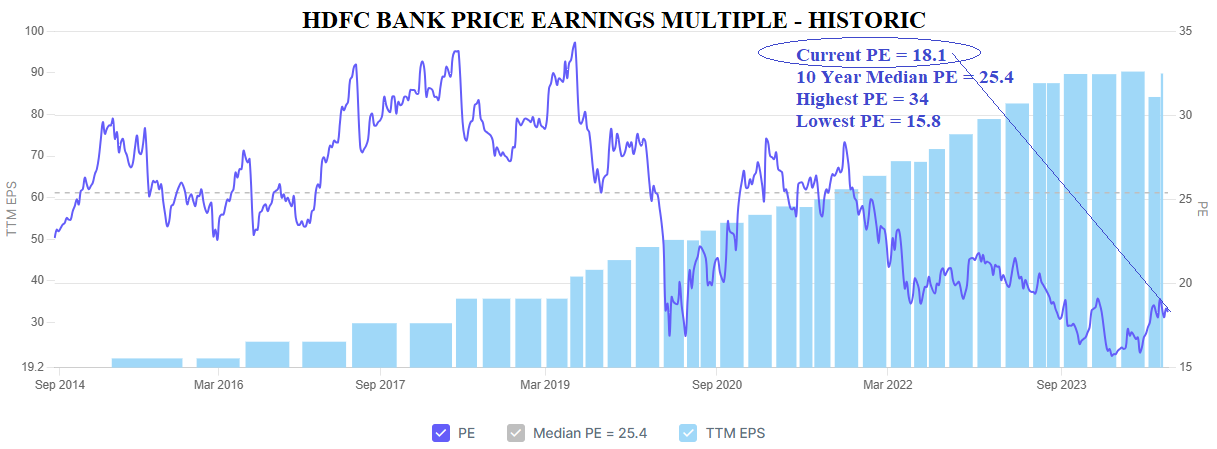

[III] HDFC is available at its lowest valuations in the past 10 years

Currently, HDFC is available at its historically low valuations. About 10 years back, HDFC Bank constantly traded around multiples of 28. Post HDFC and HDFC Bank’s merger, there were doubts around HDFC’s ability to generate high ROE particularly since the merger took place at a time when housing finance companies were struggling. This phase seems to have passed and we believe that going forward, HDFC bank will start commanding its historic premium.

[II] NET INTEREST MARGINS (NIMS)

[III] CASA RATIO

I have been avoiding private sector banks on two counts for about 3-4 years now.

First, falling CASA and term deposits. Over the past few years many new investment opportunities came about which not only offered higher interest payouts to investors but also were far more tax efficient than traditional bank deposits and FDs. The market for Debt mutual funds and Balanced advantaged funds (often mis sold as bank FD replacements) grew multi-fold over the past 5 years as more and more investors moved towards these tax efficient options. This meant lesser money for banks to advance credit. RBI governor on his part has been vocal about how skewed credit deposit ratio presents a systemic risk for banks wanting to advance more loans than they should.

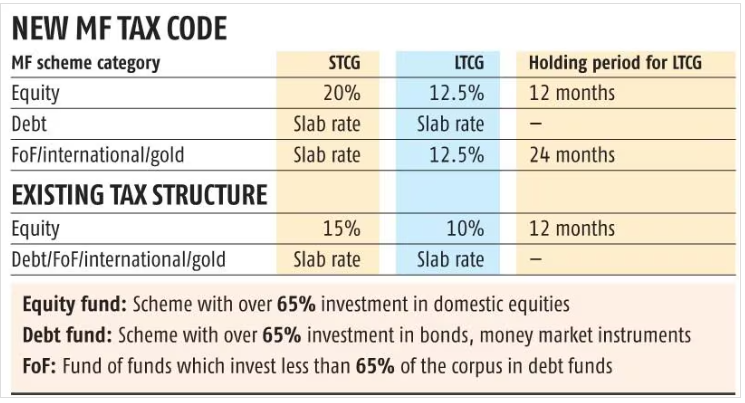

The Union Budget on 23 July 2024 changed this. There is no longer any tax advantage to investing in debt mutual funds after change in tax policy for these instruments as below.

CASA ratio and NIMs are two very decisive factors for a bank. A higher CASA ratio is preferred as it reduces the liability of the banks to pay interest on the deposits. Similarly, a higher NIM is preferred as it reflects that interest income earned is higher than the interest paid out. On both the grounds, HDFC Bank proves to be very competitive in comparison to higher valued peers

HDFC Bank Net Interest Margin

| FY 2019 | FY 2020 | FY 2021 | FY 2022 | FY 2023 | FY 2024 |

| 3.97 | 3.79 | 3.85 | 3.64 | 3.67 | 3.21 |

Further, increase in deposits will not only improve the Bank’s Net Interest Margins (NIMs) but will also help with expansion to tier III cities and beyond. Higher deposits will translate into higher net interest earnings since expenses are unlikely to go up with increasing deposits.

Also, Current Account Savings Account (CASA) growth is likely to improve with changes in tax policy. CASA deposits require very little interest payment (i.e. they are a cheaper source of raw material for the bank) and are a major boost to any bank’s NIMs.

| Figures in Rs. Crores | FY24 | FY23 | FY22 | FY21 | FY20 |

| CASA (%) | 38% | 44% | 48% | 46.10% | 42.20% |

| CASA (RS IN CR) | 908700 | 836000 | 751050 | 615682 | 484625 |

| CASA YOY GROWTH | 9% | 11% | 22% | 27% | 24% |

| TERM DEPOSITS (RS IN CR) | 1471023 | 1047406 | 808168 | 719378 | 662877 |

| YOY GROWTH | 40% | 30% | 12% | 9% | 25% |

INDUSTRY-LEADING ASSET QUALITY and RETURN ON EQUITY

Non-Performing Assets (NPA) position has improved across banking sector over the past few years on account of reduced interest rates. This however always remains a worry for banks in case of a recession and slowdown in the overall economy. When compared with best of industry players, HDFC’s NPA levels have been the best and remain so for many years.

HDFC Bank’s current net NPA 0.33% and Gross NPAs are at 1.24% which is the lowest in the industry.