Over the past week, the Hang Seng Index and the CSI 300 Index of china have experienced a dramatic reversal, transforming significant one-year declines into robust gains within days.

Market sentiment has shifted decisively from a stance of “Anything But China” to “All In, Buy China.”

Hang Seng Index Overview

As of October 7, 2024, the Hang Seng Index has posted a remarkable year-on-year gain of 31.15%, climbing by 5,456.35 points. The index now records a price-to-earnings (P/E) ratio of 13.25, reflecting a revaluation of Hong Kong-listed stocks. Historically, the Hang Seng’s P/E ratio has fluctuated between a high of 18 and a low of 7 over the past decade, with an average P/E of 11.68. With the recent upward movement, the Chinese markets, once considered undervalued, have now reached a fair valuation level, driven by renewed optimism.

CSI 300 Index Performance

In parallel, the CSI 300 Index, which tracks mainland China’s blue-chip stocks, has surged by 25% in just under two weeks. This rally was catalyzed by a series of stimulus measures introduced by Chinese financial institutions, including the central bank and financial regulators, to revitalize the nation’s stock and property markets.

The aim was to revive stock and property markets which used to constitute almost 30% of China’s GDP, which had been performing poorly: the CSI 300 lost nearly half its value from February 2021 to mid-September 2024.

The latest policy interventions signal a concerted effort to restore confidence in China’s financial markets and shore up the Real Estate sector of the economy. The rapid market recovery highlights the impact of these measures, as investors are once again looking at China with renewed enthusiasm, shifting sentiment to favor Chinese equities.

Reason Behind the Rally

China’s CSI 300 index has surged by approximately 25% in the past week, marking its largest weekly gain since the 2008 Global Financial Crisis. This rally has been driven by coordinated efforts from the Chinese government to stabilize the property market and support the broader economy and stock market.

China’s consumer economy has struggled, hindered by low consumer confidence, falling real estate prices, and liquidity issues affecting major property developers. The housing market crisis and other structural challenges have further strained the economy.

The Chinese government introduced a series of aggressive stimulus measures to address these challenges which led to China’s economic cycle showing improvement, with Q1 2024 GDP growth reaching 5.3%, exceeding the estimated 4.8%, and reflecting a +1.6% increase from Q4 2023.

Key actions included:

- Reduction in the required reserve ratio (RRR) for major banks from 10% to 9.5%, unlocking additional cash for economic growth.

- Interest rate cuts, including a 0.2% reduction in very short-term rates.

- Lower mortgage rates to support the housing market.

- Quantitative easing, with $142 billion injected into banks.

- Liquidity measures, such as loan facilities for share buybacks and a program enabling funds, insurers, and brokers to more easily purchase shares.

- Direct government intervention in buying mainland stocks to stabilize the domestic stock market and influence indices.

Additionally, foreign and local investors who had previously taken short or underweight positions in Chinese markets are returning, encouraged by improved economic sentiment, low valuations, and government actions aimed at stabilizing the economy.

Are Chinese market still Attractive?

Despite recent gains, China’s stock markets remain relatively inexpensive compared to corporate earnings. Shares have shifted from being extremely undervalued to somewhat less so, but valuations still appear low.

China’s internet sector has particularly struggled over the past three years, with the CSI Overseas China Internet Index plummeting by 70%. Despite this, most companies in the index (9 out of the top 10) have shown steady earnings growth over the last five years. Valuations remain below their historical averages and are well below those of the NYSE FANG+ Index, suggesting there could be upside potential.

China’s stock market has significantly underperformed compared to global markets and other emerging economies for over three years. This underperformance is due to several factors, including the COVID-19 pandemic, a collapse in the real estate sector, high debt levels, geopolitical tensions with the U.S. and Taiwan, an export crisis, and capital outflows.

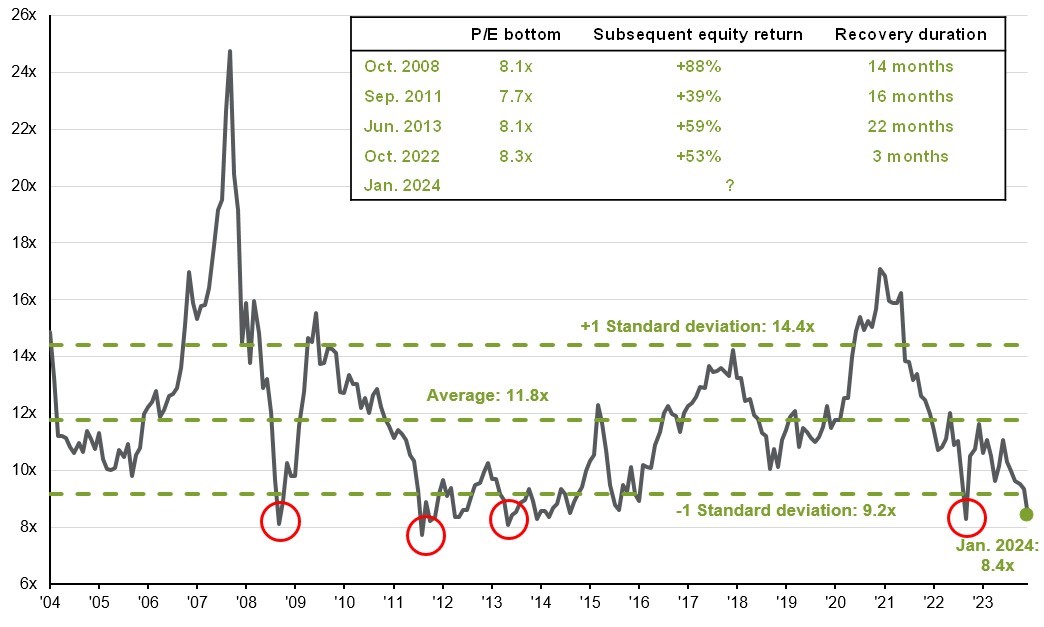

The MSCI China Index currently trades at 10.84 times forward earnings, compared to the 17.7 times average for global markets. Historically, the MSCI China P/E ratio has been lower only four times in the past 20 years—each time followed by significant tactical rebounds.

Should You Invest in China?

Despite recent stimulus efforts, investing in China still carries significant risks. One major concern is the government’s influence on business, which has stifled the technology sector since the 2021 crackdown and discouraged entrepreneurship. Geopolitical tensions, particularly with Taiwan, add another layer of uncertainty for investors.

Many remain skeptical about China’s economic outlook. While the stimulus is substantial, it doesn’t fully address deep-seated issues like the housing market, which faces excess supply and weak demand. Economists argue that China may struggle to maintain economic momentum. The sustainability of the market’s progress now depends on further government action and how effectively it stimulates domestic consumption. The key question is whether this recent boost is a one-off or part of a more serious, long-term commitment by Chinese authorities.

The bullish case for Chinese stocks rests on the possibility of additional stimulus measures, such as further reductions in the required reserve ratio (RRR), lower mortgage rates, or increased government spending. Clear signs that the economy has bottomed will also be crucial for investors.

What Should Investors Do?

China could serve as a strategic hedge for global portfolios. As one of the world’s largest and most liquid markets, it remains cheap, under-owned by international investors, and relatively uncorrelated with U.S. monetary policy. China’s stock markets move in idiosyncratic ways relative to other world exchanges, with a lower correlation to international trends. This presents a unique investment opportunity, as exposure to Chinese markets can serve as a potential hedge against volatility driven by U.S. Federal Reserve policies. Additionally, it may enhance portfolio diversification benefits.