Valuations L T Foods

L T Foods is available at cheap valuations. Company is growing revenue (19% CAGR over last 3 years) and profits (29% CAGR over last 3 years) at good rate, however, it is still valued at a PE of 16, which signifies good scope of re-rating.

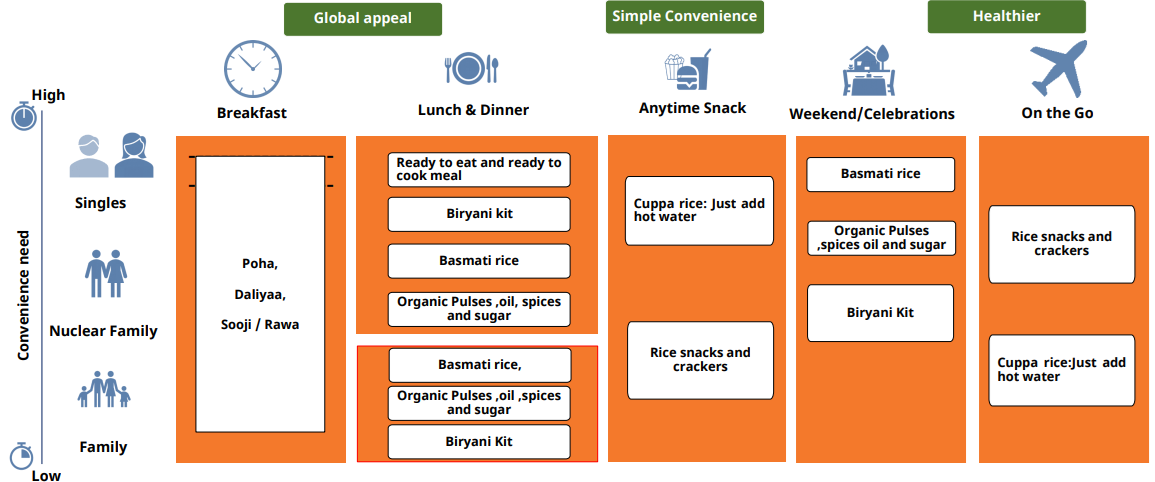

New business segments are in line with company’s current strengths and weaknesses. They use existing distribution network and cash flows to build the brand while removing cyclicity of paddy prices with branded products. Further, with increasing trend of health-conscious eating and ready to heat/cook foods with both partners working, the two segments can get good growth according to us.

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 280 | 235 (12/2023) | 106 (5/2023) | 235 (12/2023) | 2.8 (2009) | – |

| PE Ratio | 16.4 | 15.1 | 10 | 15.1 | – | 12 |

| EPS | 17.1 | 15.2 | 12.3 | 15.2 | – | – |

| Price/Book | 2.91 | 2.6 | 1.7 | 2.6 | – | 1.6 |

| EV/EBITDA | 10.20 | 9.5 | 7.1 | 9.5 | – | 7 |

| ROCE | 22% | – | – | – | – | 19% |

Financials

Snapshot of the financial

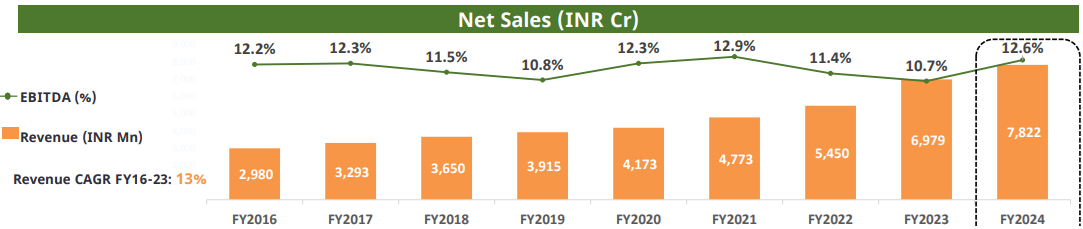

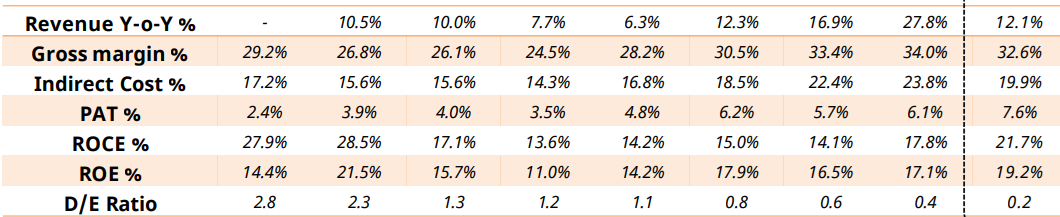

- Sales Growth: The reported sales of Rs 7772 crores are growing at a 5-year CAGR of 15% 3-Year Average Growth: 17.9%.

- Profit Growth: 5-Year Average Growth: 35.9% 3-Year Average Growth: 29.4% which is way higher than its immediate competitors.

- Operating Profit Margin (OPM): The OPM remains consistent at 11%-12%, reflecting its improving operational efficiency.

- Earnings Per Share (EPS): EPS is increasing at 5 year CAGR of 34%.

- Free cash flow yield of 6.2% compared to its competitor, Avanti Feeds, LT Foods’ Free cash flow yield is healthier.

- Debtor Days: The number of debtor days is reducing, indicating improved collection efficiency.

- Inventory Days: Inventory days have slightly increased. Days Payable: Days payable has increased.

- Cash Conversion Cycle: The cash conversion cycle is reducing, which is a positive sign.

- Return on Capital Employed (ROCE): ROCE has increased, indicating better efficiency in using capital.

- Debt Reduction: LT Foods has actively reduced its debt, thereby improving its financial and credit risk profile.

- Credit Rating: CRISIL has upgraded the company’s credit rating, reflecting increased confidence in its financial stability and future performance.

- Net Debt: Despite having high net debt, it is considered feasible within the industry context, as the basmati rice industry typically requires high inventory holding due to the aging process of paddy, which lasts 12 to 24 months.

- Current Ratio: With a current ratio of around 1.6, the company is unlikely to face difficulties in meeting its short-term liabilities, indicating good liquidity management.

- Core business: Working capital intensive (220-230 days is normal working capital), as rice must be purchased and aged for 1-2 years before sales. It also exposes company to price risk since rice purchased in up-cycle might be sold in down-cycle. Company appears to have managed both the risks well over time, given margin consistency and expansion

Conclusion:

LT Foods has demonstrated strong and consistent financial performance over the past years, with robust growth in sales and profits. The company’s strategic initiatives to reduce debt and improve its credit profile have been recognized by CRISIL’s rating upgrade. Although the industry necessitates high inventory holding and debt, LT Foods manages these factors effectively, maintaining a healthy current ratio and a feasible debt level relative to the industry standards. Overall, the financial outlook for LT Foods appears positive, with continued growth and stability expected.

Overall, the company is performing well across various aspects and remains stable, especially when compared to its competitors and peers. However, notable red flag is:

Promoter Holding: The promoter holding in the company is relatively low. Moreover, it has decreased from 56.82% to 51%, which could indicate potential concerns about the promoters’ confidence in the company’s future prospects

Soft factors for consideration:

- L T Foods has good management and has executed capex well in past

- Geographically, it’s operations are concentrated in US and India

- ~87% revenue comes from rice, and company can expect re-rating as an FMCG if the other two segments kick in

- Debt reduction is key focus for management. Business is WC intensive however, and is open to commodity price risks since there is ~1.5-2 years gap b/w buying paddy and selling rice

- Company has prudently used inorganic acquisitions to grow

- Good part of the growth has come from price growth, and to a lesser extent from volume growth. When basmati and non-basmati rice prices fell down from 2014-2017, company still managed to increase revenue by ~10% CAGR. Given that currently Basmati rice prices are at a peak, there is a chance it can fall down. However, going by past track record, good chances of management able to manage this

Management Discussion and Analysis:

Management is optimistic about achieving double-digit growth. Distribution Expansion: The company plans to increase its focus on distribution to reach more outlets. Demand Outlook: Management has a positive outlook on demand. Digital Capabilities: Investment in digital capabilities will be a priority. Product Focus: There will be a strong focus on expanding the ready-to-eat and ready-to-cook segments, particularly in the US market. Capital Expenditure: The company has announced a ₹200 crore CAPEX investment aimed at expanding its digital infrastructure.

Overview of Business

L T Foods, established in 1990, mills, processes and markets rice (largely basmati). The company has established brands such as Daawat, Royal, Devaaya, Rozana, Heritage, and Chef’s Secretz, varying from basic to premium quality, both in the domestic and overseas markets. It has facilities in Haryana, Punjab, and Madhya Pradesh, with combined milling capacity of 106 tonne per hour (tph) and individual capacity of 58 tph

Revenue Segments:

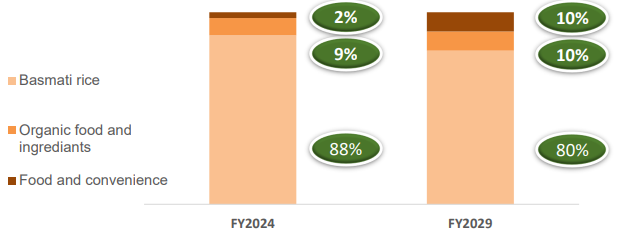

Company produces Basmati and other speciality rice (Contributing 88% of FY24 sales). They have 2 more segments, viz. Organic foods and ingredient (9% of FY24) and Ready to heat segment (2%)

Revenue and Margins:

Product Portfolio:

Competition:

KRBL is the biggest domestic player, followed by L T Foods. KRBL competes only in Basmati rice. Chamanlal Setia, Sarveshwar foods and GRM Overseas are other major competitors. LT Foods enjoys dominant position against all of them in exports, and it is catching up in domestic as well. Given Basmati industry’s domestic and global growth rates, it is clear LT Foods is capturing market share

Risk:

- Policy risk – India banned non-basmati rice exports (15% of total revenue). Similarly, US also imposed ADD on soya products from India. While ban didn’t impact the sales much, and ADD was mitigated with a facility in Uganda, company is still exposed to policy risk

- Geopolitical risk – Middle East is the largest market of Basmati rice globally. Currently, it contributes 5% of total sales but the company has future expansion plans in the region, which will be impacted owing to the ongoing wars. Also, increased freight costs have impacted profitability (Given India and Pak are the only Basmati rice producers, this impacts all players)

- Business model risk – Bulk of RM are commodities (Melamine, phenol, ethanol, kraft paper, coal, acrylic). They also carry significant rice inventory (200-220 days) and hence are exposed to rice price cycles.

-

Concerning point: They have managed to maintain 10-12% OPM over 10-12 years. KRBL, C Setia have both shown OPM fluctuations, which is expected in agro-product company where both RM and Sales are commodity prices, and 1-2 year inventory holding period is also present

-

Exchange rate risk – Since company is export oriented with bulk of paddy procured from India, currently it is not exposed to significant forex risk. However, company hedges its open exposures using derivatives.