We believe that Laurus Labs is poised to enter the club of major pharmaceutical players in India and capture a significant market share.

UPDATED REPORT ON LAURUS LABS AS OF 23-05-2024

| Valuation | ||||||||

| Particulars | FY 20-21 | FY 21-22 | FY 22- 23 | FY 23- 24 | FY 24- 25 E | FY 25- 26 E | FY 26- 27 E | |

| Profit After Tax | 983.8 | 832.2 | 793.4 | 162.27 | 505.9 | 1028.8 | 1492.3 | |

| Market Cap as on 12-05-2024 | 23582 | |||||||

| PE Multiple on FY 24-25 E | 47 | |||||||

| YOY Growth on PAT | 285.40% | -15.41% | -4.66% | -79.55% | 211.74% | 103.36% | 45.06% | |

| Assumed PEG Multiple on FY 26-27 E | 1.5 | |||||||

| Estimated PE trailing multiple in FY 26-27 E | 68 | |||||||

| Terminal Value Estimate for FY 26-27 | 100877 | |||||||

| DCF Method with Terminal Value using PE | ||||||||

| Cash Flow From Operations | 733.0 | 911.1 | 993.9 | 665.7 | 1096.8 | 1261.8 | 1575.0 | |

| Cash Flow From Investing Activities | -683.9 | -876.7 | -987.5 | -676.0 | -600.0 | -600.0 | -600.0 | |

| Net Borrowing | 391.1 | 270.2 | 221.6 | 541.1 | 100.0 | 100.0 | 100.0 | |

| Interest Paid | -58.0 | -85.0 | -140.4 | -174.3 | 0.0 | 0.0 | 0.0 | |

| Free Cash Flow to Equity | 382.2 | 219.6 | 87.6 | 356.4 | 596.8 | 761.8 | 1075.0 | |

| DATE | 31-03-2025 | 31-03-2026 | 31-03-2027 | |||||

| Cash Flows | 596.8 | 761.8 | 1075.0 | |||||

| TERMINAL VALUE | 100877.3 | |||||||

| TOTAL CFS | 596.8 | 761.8 | 101952.3 | |||||

| Cost of Equity | 18% | |||||||

| Valuation as on 23 Feb 2021 | 74463 | |||||||

| Number of Shares issued | 53.9 | |||||||

| Valuation Per Share | 1382 | |||||||

| Current Market Price | 450 |

VALUATIONS

Laurus Labs revenue has consolidated over the past year. This is primarily due to significant capital expenditure of 2600 crores in FY22-24 and operational deleverage. In future, this CAPEX will translate into revenue-generating capabilities. If the company can successfully convert these CAPEX investments and increase its Asset turn from 0.9 to 1.4, we could potentially see an additional revenue of Rs. 3300 crores in FY25-27. Furthermore, if operating leverage also comes into play, the revenue could increase substantially in the coming years.

From the current level of 438 Rs, we believe the share price has the potential to reach the level of 1300 in next 3 years.

| Income Statement (INR in Crores) | ||||||

| Particulars | FY 21-22 | FY 22- 23 | FY 23- 24 | FY 24- 25E | FY 25- 26E | FY 26- 27E |

| Revenue from Operations (Net of Excise/GST) | 4,935.57 | 6,040.55 | 5,040.83 | 6,524 | 7,727 | 9,834 |

| Cost of Goods sold (COGS) | 2193.8 | 2774.3 | 2432.4 | 3066 | 3554 | 4524 |

| Other expenses – reclassified as Manufacturing Expense | 545.02 | 761.57 | 833.69 | 1044 | 1004 | 1180 |

| GROSS PROFIT | 2,196.8 | 2,504.7 | 1,774.7 | 2,414 | 3,168 | 4,130 |

| Other Expenses – Reclassified as non- Manufacturing Expense | 272.83 | 331.84 | 357.29 | 391 | 386 | 492 |

| Employee Benefits Expenses | 501.53 | 580.64 | 639.93 | 718 | 773 | 885 |

| Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA) | 1,422.4 | 1,592.2 | 777.5 | 1,305 | 2,009 | 2,753 |

| Depreciation and Amortisation | 251.49 | 324.08 | 384.58 | 456.70 | 463.60 | 590.03 |

| Other Income | 13.58 | 1.44 | 26.34 | 26.34 | 26.34 | 26.34 |

| Finance Income | -1.72 | -4.56 | 0 | 0 | 0 | |

| Finance Expenses | 102.39 | 165.17 | 182.9 | 200 | 200 | 200 |

| Profit Before Tax | 1,083.8 | 1,108.9 | 236.4 | 674.5 | 1,371.7 | 1,989.8 |

| Income Tax Expense | 251.42 | 312.30 | 68.15 | 169 | 343 | 497 |

| Share of results of associate | 0.2 | -3.2 | -5.9 | 0 | 0 | 0 |

| Profit After Tax | 832 | 793 | 162 | 506 | 1,029 | 1,492 |

| EPS | 9.385277 | 19.08629 | 27.68738 |

| Vertical Analysis _Segment Revenue | FY 22- 23 | FY 23- 24 | FY 24- 25E | FY 25- 26E | FY 26- 27E |

| API-ARV | 27% | 30% | 23% | 19% | 15% |

| API- Onco | 4% | 8% | 10% | 10% | 10% |

| API- Other | 12% | 12% | 12% | 12% | 12% |

| FDF- ARV | 12% | 19% | 15% | 13% | 10% |

| FDF- NON ARV | 7% | 9% | 16% | 16% | 17% |

| CDMO | 36% | 18% | 20% | 25% | 30% |

| BIO | 2% | 3% | 4% | 5% | 6% |

| TOTAL | 100% | 100% | 100% | 100% | 100% |

The major growth expected in Laurus will come from the CDMO and Bio business, boosting the margins. Laurus CDMO business will go from 18% to 30% and Bio from 2% to 6%, taking the EBITDA margin from 15% in FY24 to 28% in FY27.

What played out well for Laurus Labs

Diversification – Laurus Labs successfully validated its thesis

Execution of management to scale the new business lines & transform the business from a pure-play API player to a diversified pharma company

Over the past 6 years, Laurus Labs went from a single-product company with a dominant market share in Antiretroviral Active Pharmaceutical Ingredients (ARV-API) to diversifying through Formulations, CRAMS (Contract Research and Manufacturing), and also among other verticals (discussed below).

- While the ARV segment’s share in total revenue has declined from 65% in FY2018 to 37% in FY2023, this traditional busiess now contributes Rs. 2,235 crores to the total revenue as commpared to Rs. 1,336 in 2018.

- CDMO Synthesis (Contract Development And Manufacturing Organization) now contributes about 36% of revenues (i.e. Rs. 2,175 crores.

- APIs other than ARV i.e. focusing on cancer therapy (Oncology), anti-allergic, cardiovascular, diabetes, asthma, and heart diseases, etc. contribute 18% to the revenue or Rs. 1,087 crore.

- Biotechnology segment currently constitutes a modest 2% of the company’s overall portfolio or Rs. 120 crore. Laurus Labs is strategically positioned to bolster its presence in Biotechnology by allocating capital expenditures for future expansion and growth.

Laurus Labs relied heavily on the production of ARV-APIs focusing on the treatment of Human Immunodeficiency Virus (HIV). However, the growth in HIV drugs is slowing down so Laurus initiated its diversification efforts away from APIs into formulations and the manufacturing of Key Starting Materials (KSM) and Intermediates.

Let’s explore how Laurus Labs’ diversification away from ARV APIs has positively impacted its business performance.

1.Active Pharmaceutical Ingredients(APIs):

Laurus Labs is one of the largest API players in the ARV drugs (HIV) market.

Laurus develops, manufactures, and supplies APIs in high-growth therapeutic areas of Anti Retro Viral (ARV), Oncology, and Hepatitis C to formulation companies in Latin America, Southeast Asia, and Sub-Saharan Africa markets, which are typically the fast-growing donor-funded access-to-medicines markets.

1(a) Anti Retro Viral (ARV)- As of the end of 2022, 29.8 million people with HIV were accessing antiretroviral therapy (ART) globall (this is 76% of all people with HIV).

The patents which expired on the ARV side in US & EU markets presented an opportunity for Laurus.

- Laurus has Signed a Supply agreement with The Global Fund for ARV drugs for the 2023-2025 period

Laurus Labs has secured the United States Food & Drug Administration (US FDA) approval for the World’s First Paediatric ARV Oral Dispersible Film (ODF) drug, Dolutegravir 5mg and 10mg in HIV/AIDS treatment- For children

Earlier, Laurus Labs also became the first generic approved company for a fixed dose combination of Abacavir/Dolutegravir/Lamivudine 600/50/300 mg, which is being used to treat adult HIV patients.

Laurus launched a Dolutegravir-based combination of Tenofovir + Lamivudine + Dolutegravir (TLD) in South Africa with Aspen after shifting from Efavirenz-based therapy to Dolutegravir-based therapy.

Some other manufacturers of dolutegravir –

Cipla, Mylan, Aurobindo Pharma Mangalam Drugs & Organics, etc.

What Makes Laurus Labs Different?

Laurus Labs faced a challenge when shifting from Efavirenz to Dolutegravir-based therapy. Dolutegravir required only 50 mg, which was a 12 times reduction in API quantity. To overcome this, the company created the manufacturing capacity of Dolutegravir in advance. This helped Laurus Labs to become a formulator of ready-to-consume triple combination drugs (DLT) rather than just a simple API supplier.

(b)Hepatitis C – In FY 18, Laurus Labs partnered with Natco Pharma to create and market a Hepatitis C-related product, with the net profit from its sale being shared by the two companies

HepC business has not grown much in the past few years. The company is focused on trying to increase Oncology API business

(c)Oncology API (focusing on cancer therapy) – The oncology API is a low-volume, high-value API business.

Lauras has strengthened global leadership in Oncology.

Dr. Chava (Promoter, Laurus Labs) claimed that Laurus has the largest Onco API capabilities in the country.

Some of the key suppliers in the API market include Scino Pharma, Shilpa Medicare, and MSN Laboratories.

2. Formulation (FDF): The forward integration that Laurus Labs has done in the API space by making off-patent drugs for sale has pushed Laurus to a higher level in the pharmaceutical value chain. In Formulations Lauras Labs manufactures ready-to-consume drugs and sells them in the market.

Formulations have better margins than APIs and give Laurus Labs a more sustainable market share- In Formulations, Laurus has an in-house API facility which has helped them earn a higher profit margin for Finished Dosage Forms (FDFs).

Laurus’ oral finished dosage facility in Visakhapatnam has a commercial capacity of 10 billion units but is currently operating at 5 billion units, with the potential to increase to 7 billion units by year-end. The FDF business aims to position the Company as a top provider of integrated solutions globally.

Currently, Major growth in Formulations is driven by ARV but the management thinks that both ARV APIs and Formulations will attain their peak revenues soon.

Growth in formulations for future quarters will come from non-ARV, as indicated in the Capex plan presented by management (discussed below).

Management Guidance: (Q1 FY24 CONCALL)

Formulations segment has a strategic emphasis on three primary sectors:

- Distributing antiretroviral (ARV) drug formulations and providing non-ARV medications to lower and middle-income countries (LMIC) which is a Tender driven business – Tender driven businesses are considered to be lumpy and highly competitive. Prominent organizations issuing such tenders include PEPFAR and the Global Fund.

- Specializing in the production of formulations for clients in Europe and other advanced markets.

- Marketing non-ARV drug formulations under their brand labels in the United States and other developed regions.

The FDF business has grown at a CAGR of 114%. Laurus has been able to increase the share of Formulations without any cannibalization in its own API business.

3.CDMO Synthesis(Contract Development And Manufacturing Organization): CDMO is a high-volume and high-margin business.

Before getting into nitty- gritty of this segment let us understand what CDMO segment as a business is and why Laurus is betting huge on CDMO.

The chart above serves as a comprehensible illustration of the CDMO (Contract Development and Manufacturing Organization) concept.

In CDMO the company partners with other pharmaceutical companies to help them create and bring a new drug to the market. This collaboration covers everything from developing the drug to getting it out there for people to use

- The company does custom synthesis for global companies such as C2 pharma & Aspen (Aspen is one of the top ten largest generic manufacturers in the world)

- The unit 5 of the company is dedicated to manufacture custom APIs for Aspen

Management asserts that their core strategy revolves around forming strategic collaborations with pharmaceutical companies that are in the advanced phases of clinical trials, namely Phase 2 and Phase 3. This mitigates the risk of drug failing in the development process.

Laurus provides contract manufacturing services to generic pharmaceutical companies. While the technology and DMF(Drug Master File) remain under their ownership. Laurus offers their manufacturing capabilities at a predetermined margin. This business model is advantageous due to cost predictability, process consistency, and capacity expansion. Laurus offer to their partners, essentially providing comprehensive manufacturing solutions.

(Below is Concall Snapshot of Q4 FY23)

Management has guided that majority of capex will be done for CDMO(Synthesis) and BIO division

The management has long term vision for CDMO business. The chances of gross margins increasing beyond 52% will certainly go up if CDMO starts contribution in a meaningful way.

4.Laurus Bio (High margin business gross margins of about 70%)

Biotechnology has opened up exciting possibilities for Laurus Labs. Laurus aims to grow its market share by investing in disruptive technology, building niche capabilities, and the implementation of backward integration, all aimed at enhancing operational efficiency.

In FY2021, Laurus Labs Ltd acquired Richcore Lifesciences Pvt. Ltd which is now called Laurus Bio

The project was Green field, and the acquisition gave Laurus Labs Ltd access to recombinant technology, something they did not have before. Moreover, this strategic acquisition saved them nearly 6-7 years that they would have needed to develop the technology in-house.

Laurus offer in-depth fermentation based product development and manufacturing expertise, as a service (CDMO) to novel protein companies and bio-manufacturers

Long-term outlook for the Bio segment is that expansion will reach 1 million litres fermentation capacity.

BIOTEC – POTENTIAL FUTURE GROWTH DRIVERS – ALPHA CREATION

CAPEX & RECENT INVESTMENT OF LAURUS LABS IN BIOTEC SPACE:

An investment of up to 10% of profits in disruptive technologies has led to:

- Increased stake in Cell therapy company “ImmunoACT” to 34% (curing specific types of blood cancers). CAR-T treatment (a cancer treatment specialised by ImminoACT) is being expanded to service more patients. This treatment reduces treatment cost of cancer from ~ Rs. 1 Crore to ~ Rs. 15-30 Lakhs.

- Collaboration with IIT Kanpur to inlicense and fund development of Gene therapy assets

ImmunoAct – Laurus Labs’ associate is presently incurring losses, and these losses are reflecting on Laurus as well. However, the management has a clear strategic vision for achieving profitability by transitioning Immuno’s products into the commercial phase.

The existing facility has the capability to accommodate 500 treatments annually, while the company is diligently working towards completing a new facility, expected to be operational as early as 2025, which will substantially enhance treatment capacity to 3,000 treatments per year.

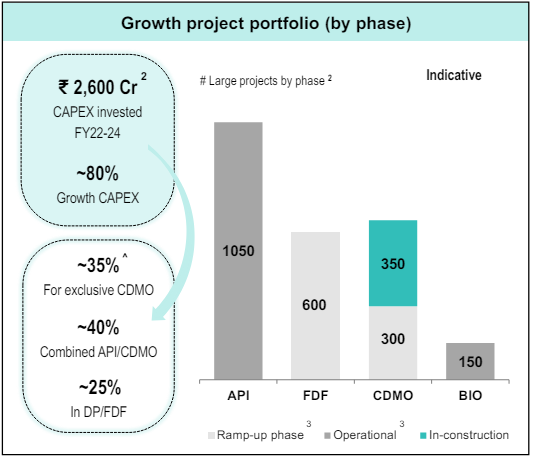

Examining the capex guidance for FY22-24, the management has done capex of INR 2600 crores in capex, financed through internal accruals and borrowing. In FY23, the company is undergoing a consolidation phase, during which the management is dedicated to seizing every viable opportunity for capacity expansion, aimed at supporting all segments of their business. The anticipated outcomes of these efforts are expected to become evident starting in FY25

Laurus has cumulatively invested over Rs. 2600 crore since FY22. Capex guidance has remained 16-17% of Revenues. Large part of Capex addition between FY22-24 was mainly in Non-ARV infrastructure (FDF & API division) which is under ramp-up phase.

Strong focus on Research & Development by Laurus Labs Ltd:

Laurus has always focused on Research & Development and has been spending about 4%-7% of its sales on R&D. A large spending on R&D has helped it achieve a global leadership position in its products and a long-term relationship with its customers like Aspen, Mylan, Aurobindo Pharma, Natco, Sun Pharma, and Cipla

Key Risk in Laurus Labs

- Raw Material – India is the third largest producer of API accounting for an 8% share of the global API industry. Even if the APIs are manufactured locally, the key starting materials (KSMs) are still predominantly sourced from China. The Chinese API industry accounts for 40% of the global API requirement and is supported by benefits like higher economies of scale, subsidies and fiscal incentives offered by the government and lower power, fuel and borrowing costs.

- US Regulatory Concern The U.S. continues to be an important market for Laurus Labs, with a sizeable amount of revenue coming from the region. In the last few years, the US Food and Drug Administration (USFDA) has raised red flag during its inspections on Indian manufacturing facilities. This has impacted exports to the U.S. (where Indian pharma companies have much exposure) and product approvals. Other factors like increasing competition, new ANDA (abbreviated new drug approvals), consolidation of channel partners, price erosion are other major reasons behind the downfall of the Indian pharmaceutical companies.

- Promoters’ Personal Investments in the Company The promoters of the Company, namely Dr. Satyanarayana Chava, Mr. V. V. Ravi Kumar, and Dr. Lakshmana Rao C V have also invested in Immuno Act in their personal capacity as well.

- Key-Man Risk Currently the promoter of the company Dr. Satyanarayan Chava is independently running the show for Laurus.