MANORAMA INDUSTRIES

Manorama Industries has delivered a stellar ~340% return over the past 2 years — a rally that may seem like a missed opportunity for many retail investors. But we believe the story is far from over. In fact, the next leg of value creation might just be getting started.

Global Cocoa Butter Equivalent (CBE) Market in Hypergrowth

The CBE market is expected to more than double from $1.48 billion in 2024 to $3.34 billion by 2032, growing at a 6.27% CAGR.

This is being driven by rising demand from chocolate and confectionery majors seeking cost-effective, sustainable alternatives to natural cocoa butter.

Manorama’s Market Share Could 6x

Manorama currently holds just ~2% share in the global CBE market. Given its R&D strength, backward-integrated model, and upcoming capex, we believe it can scale this to ~12% over the next 5 years — unlocking massive operating leverage.

Financial Trajectory: Steep Curve Ahead

5-year Future growth profile:

- Revenue CAGR: ~33%

- EBITDA CAGR: ~42%

- PAT CAGR: ~46%

Despite these growth rates, the stock trades at ~60x forward P/E — pricey at first glance, but fair in the context of its premium trajectory and margin re-rating potential.

Here’s why we remain bullish:

The next leg of growth appears even more promising, backed by strong tailwinds and bold execution.

Manorama Industries is quietly building the most potent value chain in the global Cocoa Butter Equivalent (CBE) space — a structurally undersupplied, high-margin niche exploding in relevance as cocoa prices skyrocket and global FMCG majors scramble for cost-effective, sustainable, and regulatory-compliant alternatives.

The global cocoa supply chain is in deep disarray — climate volatility, disease outbreaks, illegal mining, and geopolitical tensions have driven cocoa prices to historic highs (~$10,000/MT in April 2024, still hovering above $8,000). With Ghana and Côte d’Ivoire (80% of global cocoa) seeing yield collapses >20%. This leading to the demand for Cocoa Butter Equivalents to unprecedented levels.

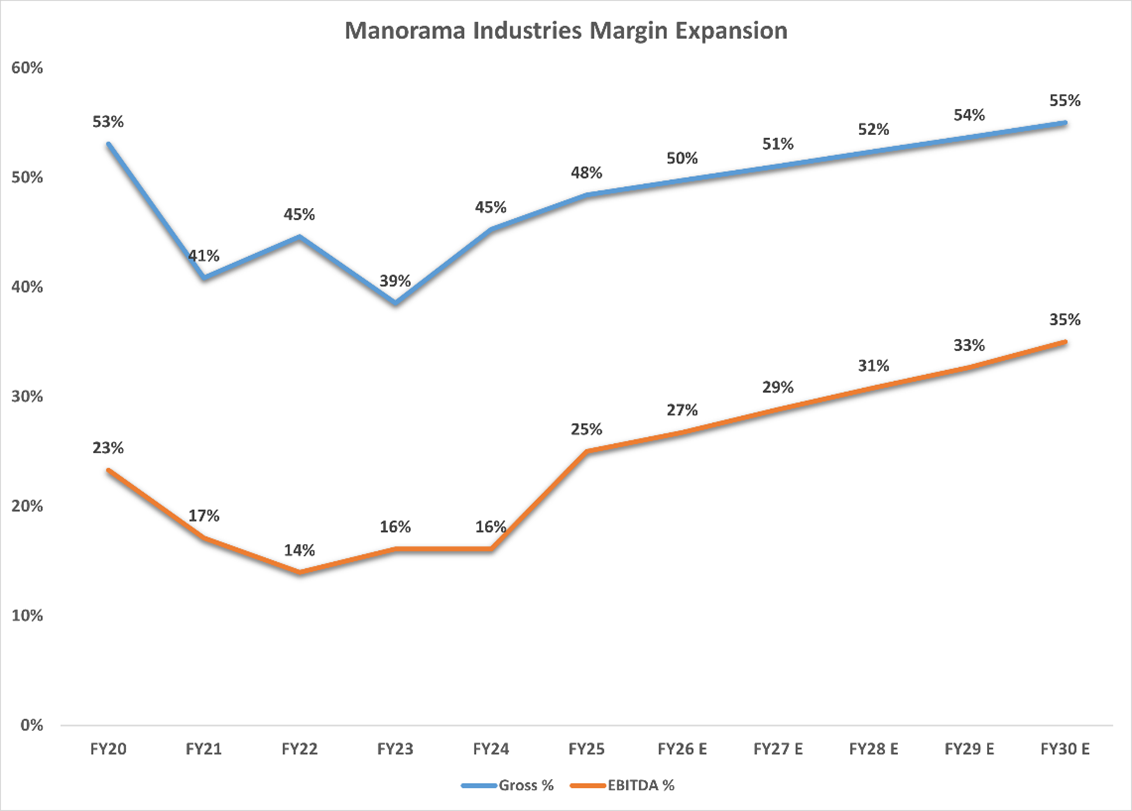

To capitalize early on the accelerating demand trend, Manorama has announced a strategic capex initiative aimed at deepening its value chain integration. This move is expected to drive significant operating leverage. We estimate this could lead to a gross margin expansion of ~500 basis points, EBITDA margin improvement of ~1,000 basis points, and a sharp rise in ROCE by ~1,700 basis points—reflecting both improved realizations and higher capital efficiency.

Backward integration project of solvent extraction for Sal, Mango and other Indian exotic seeds in Chhattisgarh, India

Indian Solvent Extraction Plant (Currently Outsourced)–

Currently using outsourced facilities for Solvent extraction in India → Paying conversion fees + transport + delays + less process control.

Impact of In-house Plant:

- Eliminate outsourcing cost (conversion + margin charged by vendor) → shows up as “Processing Charges in P&L.

- Improve gross margins as now extraction is internalized.

- Gain better control over efficiency/yield.

- Faster turnaround = lower working capital needs (indirect margin tailwind).

- Reduces COGS per kg of extracted oil.

Backward integration by creating a Pre-Phase and solvent extraction facility in the West African state of Burkina Faso

Burkina Faso Shea Nut Pre-Processing & Butter Extraction

Current Pain: Shipping raw shea nuts to India → High logistics cost (bulky, ~45–50% is waste/seed shell).

New Model: Backward integration plan to extract Shea Butter at source in Africa and ship the butter, not the nuts.

Process locally → Import only butter (high-value dense extract).

Impact:

- Massive logistics cost savings per ton of actual usable product.

- Lower inventory volume per value → Less warehousing cost, quicker conversion.

- Possibly qualifies for tax or duty benefits as processed product.

Reduce cost per ton of input & logistics burden, improving Gross/Ebitda margin.

Forward integration of manufacturing of Palm mid-fraction, which is used to make CBE

Palm Mid Fractionation → Core input for CBE: (Currently Outsourced)

Current Pain: Buying pre-fractionated palm mid from processors → Paying them for Equipment + Energy + Vendor margin.

In-House Fractionation:

- Eliminate outsourcing cost (conversion + margin charged by vendor)

- Reduces dependence on third parties.

- Internalizes the value-add margin of fractionation.

- Can optimize blend ratios better for CBE formulation.

- Higher quality control and possibly better yield.

Direct COGS saving + Better Ebitda Realization/Ton.

Another key benefit is the significant reduction in working capital pressure, particularly from previously elevated inventory days — a major area of concern.

|

Particulars |

FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | FY27 | FY28 | FY29 | FY30 |

|

Non-Cash WC Days |

286 |

255 | 274 | 209 | 336 | 313 | 300 | 288 | 275 | 263 | 250 |

|

ROCE |

17% | 13% | 10% | 13% | 10% | 19% | 24% | 27% | 29% | 32% |

36% |

What it means:

- Faster Conversion from raw material to finished goods

→ Less time in WIP (Work-in-Progress) and Finished Goods Inventory - Reduced Transit Time for Raw Material

→ Especially in Burkina Faso: bringing Shea Butter instead of Shea Nuts

→ Smaller volume, denser product, no waiting for outsourced extraction

→ Lower raw material inventory held in India - No queue or bottleneck with third-party processors

→ In-house gives better planning and control

→ Inventory doesn’t sit idle waiting for outsourced processing slots

Impact on Working Capital Days:

| Component | Impact |

| Raw Material Days | ↓ (faster input use) |

| WIP Days | ↓ (in-house speed) |

| Finished Goods Days | ↓ (more agile) |

End Result:

- Inventory Days ↓

- Overall Working Capital Days ↓

- Working Capital Cycle Shortens

- Cash Conversion Cycle Improves

This unlocks cash flow, improves RoCE, and reduces dependence on working capital loans enhances Net Profitability.

Forward integration by entering the Cocoa Butter Alternative market

Margin Expansion: Higher realizations per unit directly boost Gross Margins

- Convert Low Value Product e.g Olein (a by-product of fractionation) → High-Value Fats (like Stearin, specialized hard butters, or CBA components)

- Enhancing low-value by-products olein into high-value stearin-based products boosts realizations.

- Proprietary in-house technology reduces dependency on third parties.

Asset Efficiency Improvement → improves Sales/Asset and RoCE

Better utilization of existing fractionation units and R&D capabilities.

Strengthening Value Chain:

- Captures more value downstream by converting base/intermediate fats into finished functional alternatives.

- Reduces exposure to commodity price cycles and increases bargaining power with buyers (chocolate & confectionery companies).

Defensibility via Technology:

In-house, proven lab-to-pilot scale tech acts as a technical moat, making it difficult for competitors to replicate easily.

Forward integration by starting production of industrial and compound chocolates.

Margin Expansion Potential

- Shifting closer to B2B/B2C value chain enables capturing brand/distribution margin, not just ingredient margin.

- Uses internally produced CBA as input → creates captive consumption loop → improves blending margins.

Asset Efficiency / RoCE:

- Initially asset-heavy with working capital needs (especially inventory & receivables), but once stabilized, could deliver higher throughput per rupee of capital employed.

- Likely to improve fixed asset turnover integrated with existing CBE production.

Value Chain Deepening:

- Complete vertical integration: From seed → butter → CBE → compound chocolate → branded/industrial supply.

- Strategic shift from ingredient supplier to full-stack solution provider to FMCG and confectionery firms.

Key Risk – Direct Market Competition with Customers:

- Enters space with strong incumbents (e.g., Barry Callebaut, Mondelez suppliers, local players).

- Manorama will need to build distribution, brand trust, and scale to match pricing power.

- Execution risk high: success depends on commercial ramp-up, not just technology or ingredients.

Manorama isn’t just a CBE supplier. It is a fully-integrated exotic fats platform, with:

- R&D-led defensibility

- Capital-efficient capex (payback <3 years)

- Optionality to expand into FMCG B2B chocolate spaces

- Tailwinds from global sustainability and cost-substitution mandates

As large FMCG clients seek secure, compliant, and consistent CBE sourcing amidst cocoa chaos, Manorama emerges as a critical enabler.