In the ever-evolving world of pharmaceuticals, very few companies strike a balance between aggressive R&D, specialty product focus, and financial consistency. Yet, Natco Pharma stands out.

-

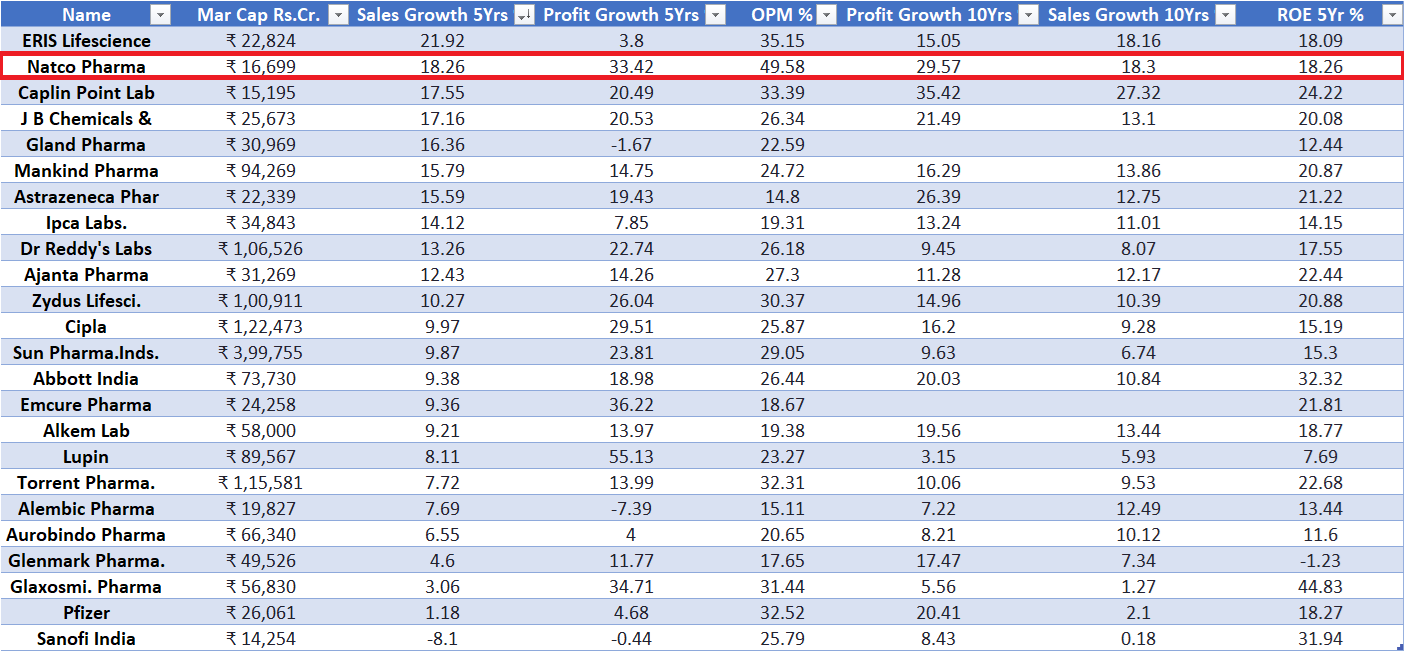

It ranks #2 among India’s leading pharma players in 5- and 10-year sales growth.

-

It ranks #4 and #2 in 5- and 10-year profit growth, respectively.

-

It commands the highest Operating Profit Margin (OPM) among peers, at nearly 50%.

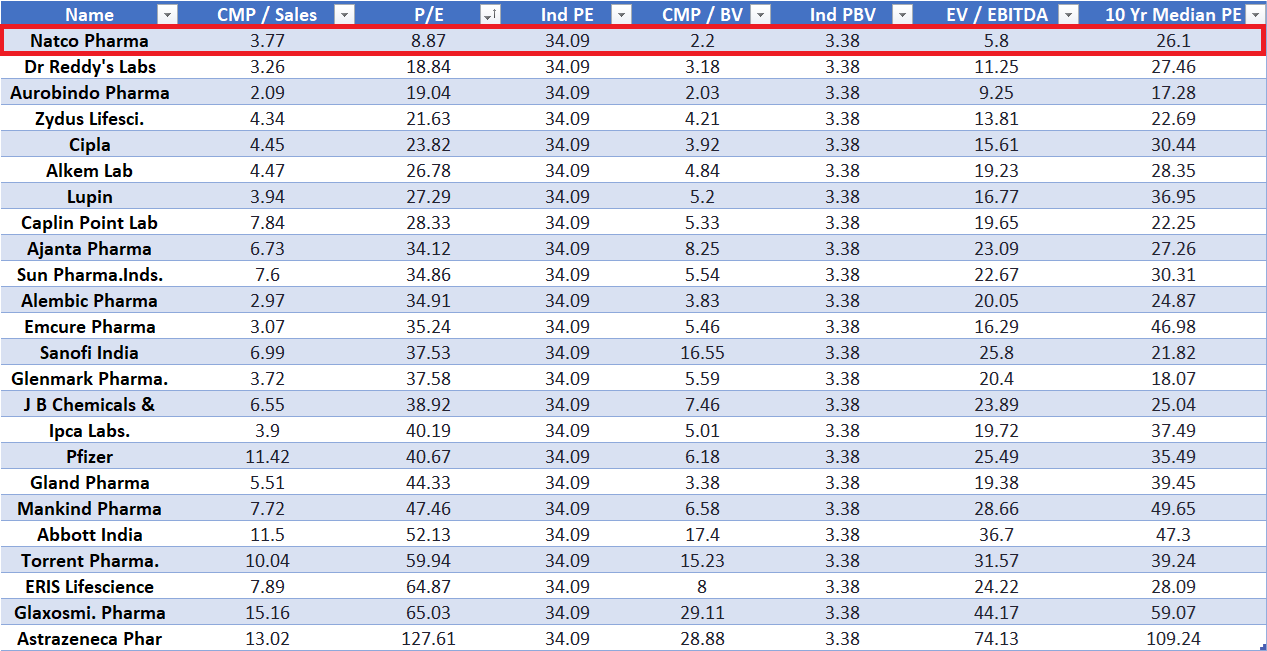

And despite all this, Natco is trading at the cheapest valuation multiples in the entire industry.

At a P/E of just 8.87x, EV/EBITDA of 5.8x, and well below its 10-year median P/E of 26.1x, the market seems to be heavily discounting something.

So what gives?

Why is a company with:

-

Consistent long-term profitability

-

A sharp focus on high-margin oncology and niche opportunities

-

Aggressive ANDA and Para IV pipeline in the US

-

Multiple sole and shared FTFs (first-to-file exclusivities)

-

And a solid track record of monetizing complex opportunities (like Revlimid)

… trading at valuation levels typically reserved for structurally broken or low-growth firms?

In this blog, we’ll dig deep into:

-

The core of Natco’s business model

-

Its growth levers and why profitability remains robust despite volatility

-

Why market perception may be short-sighted

-

And whether this deep discount presents an opportunity or a value trap

Natco Pharma Business Model

About the company

NATCO Pharma Limited (NATCO) is a vertically integrated, Research and Development focused pharmaceutical company engaged in developing, manufacturing, and marketing complex products for niche therapeutic areas.

NATCO has established its presence in three business segments viz. finished dosage formulations (“FDF”), active pharmaceutical ingredients (APIs), and Crop Health & Contract Manufacturing Business.

Business Segments

- Export Formulation: The company manufactures and markets finished dosage formulations in 50+ countries, including the US, Canada, Brazil, and Europe. Major US partners include Sun-Ranbaxy, Aceto-Rising, Alvogen, Teva, Mylan, Actavis, Lupin, etc. Its international business focuses on Para IV and first-to-file molecules, with plans to expand into emerging markets like MENA, LATAM, and Southeast Asia.

- Domestic Formulation : The domestic formulations business targets Oncology, Specialty Pharma, Cardiology, and Diabetology therapeutic areas. It has a specialized sales team of 850+ people and 1,000 distributors. The company plans to launch 5+ new products annually across 4 divisions. It is one of the leaders and pioneers in the branded oncology targeted therapy segments.

- Active Pharmaceutical Ingredients: The company specializes in niche API manufacturing, having a portfolio of 50+ APIs mainly in the oncology segment. It is also present in other therapeutic areas like Central Nervous System (CNS), pain management, and cardiovascular (CV) care. It has filed 58 DMFs, of which 49 are active.

- Crop Health Sciences: The company offers a broad range of crop protection products, including insecticides, fungicides, herbicides, biostimulants, and semiochemicals. Its key products target pests affecting crops such as paddy, sugarcane, cotton, tomato, chili, and soybean, and include technical formulations like Chlorantraniliprole, Thiamethoxam, and Fipronil.

- Other: The company is a leading contract manufacturer for 40+ pharma products, supplying major Indian companies. It offers tablets, capsules, and injectables across key therapeutic areas such as oncology, antivirals, and cardiology.

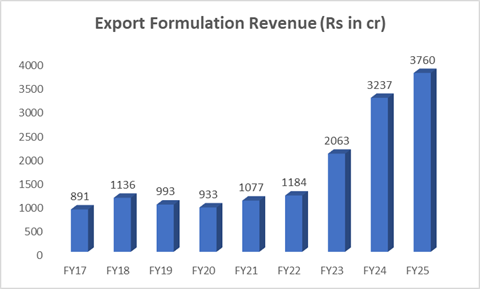

Deep Dive in Export Formulation business segment (~85% Revenue FY25) -The Real Growth Driver

Natco engages with marketing partners who are responsible for the litigation process and marketing of products.

Example-

- Partnered with Alvogen for Oseltamivir (Tamiflu) in 2016

- Partnered with Mylan for Glatiramer Acetate (Copaxone) in 2017

- Partnered with Teva for Lenalidomide (Revlimid) in 2021

Why does Natco partner with companies for US business?

- Cost Sharing and Risk Mitigation – Filing a Para IV molecule involves various fees like Filing fees ($230K), Legal and Patent Analysis Costs (ranging from $500K to a few million), Litigation costs ($5 million to over $10 million). Therefore, partnering helps Natco to share these costs.

- Distribution and Marketing Capabilities – Partner companies like Mylan, and Teva already have established distribution channels and marketing expertise which help Natco to market effectively and quickly. Natco generic Revlimid is sold under the brand name of Teva in US markets and Teva is responsible for marketing the drug.

The Hatch-Waxman Act

Natco Pharma’s export engine is largely powered by the provisions of the Hatch-Waxman Act, a U.S. law designed to balance two conflicting forces in the pharma world — innovation and affordability.

Here’s how it works: innovator companies are granted up to 20 years of patent protection, giving them time to recover R&D investments. As the patent nears expiry, innovators often file for patent extensions, delaying generic entry. However, under the Hatch-Waxman framework, generic players can file an Abbreviated New Drug Application (ANDA) and challenge weak or expiring patents — a process known as a Para IV filing.

If the generic challenger is successful and is the first to file, they are granted 180 days of market exclusivity — meaning no other generic can enter the market during that period. This allows the first filer to sell at a premium (albeit still below the innovator’s price) and capture outsized profits during this window.

This is the core of Natco’s strategy:

✔️ Focus on complex, high-value molecules

✔️ Aim to be first-to-file (FTF)

✔️ Partner with global firms for litigation and marketing

✔️ Enjoy 180-day exclusivity and outsized margins

However, this strategy has its drawbacks. The revenue profile is inherently lumpy — driven by legal wins, product launches, and exclusivity periods. There’s little room for steady, predictable earnings. As such, the company is always on the hunt for the next big molecule, and its success hinges on maintaining a robust, forward-looking pipeline.

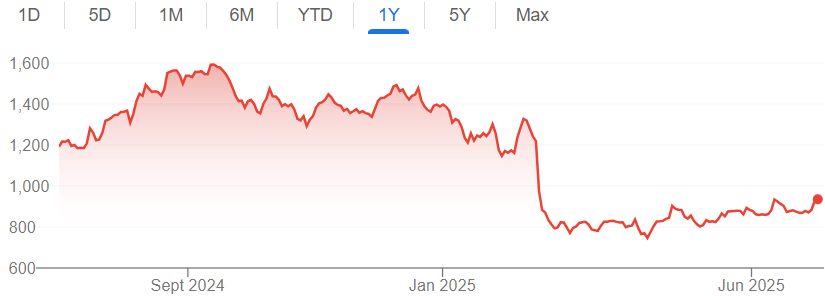

So Where Does the “Lumpiness” Come From?

You make big money during the exclusivity window, but once the market opens up, prices collapse.

Just take a look at this chart:

Within a year or two of patent expiry, drug prices fall by more than 50–70%. That’s just how this industry works. And that’s where the earnings volatility comes from.

Let’s rewind to 2022. That was Natco’s moment of glory. The company, in partnership with Teva, launched the first generic of Revlimid — one of the world’s top-selling cancer drugs. It was a massive win, both in terms of revenues and margins. The numbers started reflecting from FY23, and the stock rallied.

But here’s the thing — Revlimid was never going to be forever.

Q2 FY25 CONCALL- Natco Pharma

During the Q2 FY25 earnings call, management clearly indicated that with Revlimid’s patent expiry coming in January 2026, a major price erosion is expected. Natco has always acknowledged the lumpiness of its business. That’s the trade-off of playing in the high-risk, high-reward Para IV space.

But what really spooked the market was Q3 FY25. Why?

Because the entire year’s quota of Revlimid had already been delivered to Teva in Q2.

That meant zero Revlimid sales in Q3, and suddenly, no near-term triggers were in sight. The stock took a beating.

But honestly, this shouldn’t have come as a surprise. This is how Natco’s model works.

Boom, Bust, Repeat — Part of the Game

Natco’s revenue model is cyclical, not linear. Big windfalls driven by key product launches followed by lean years as exclusivity ends and competition intensifies. — that’s been the pattern:

-

FY2017: A revenue spike driven by the launch of Tamiflu (a ~$500 million opportunity), followed by a drop once exclusivity expired.

-

FY2022–24: A strong growth phase on the back of the Revlimid launch.

-

FY2026: Anticipated decline as Revlimid faces full generic competition.

Rather than asking how much Revlimid revenue will decline, the more strategic question is:

What does Natco have lined up next in its pipeline to sustain growth beyond Revlimid?

Q4 FY24 CONCALL- Natco Pharma

What Natco lacks in near-term triggers, it more than makes up for with its long runway of complex, high-value opportunities.

From sole First-to-File (FTF) rights on blockbuster molecules like Semaglutide (a $15B+ market) and shared FTF on Risdiplam, to medium-term bets like Olaparib, Erdafitinib, and Capmatinib.

But it doesn’t stop there.

The company is also placing early bets in New Chemical Entities (NCEs) and Cell & Gene Therapies — areas that may not generate immediate cash flows, but have the potential to be game-changers in the next decade. NRC-2694, their proprietary molecule for head and neck cancer, is already in Phase II trials with promising data. Their investment in eGenesis, a trailblazer in xenotransplantation, further underscores Natco’s willingness to think beyond generics.

In total, the company is building a pipeline of ~15 future-facing products. Even if half of them succeed, the impact could be significant — both for Natco and its shareholders.

Optionalities

With over ₹3,500 Cr in cash on the books, Natco Pharma is sitting on a serious war chest. The management has already hinted at potential acquisitions over the next 12–24 months — a move that could help cushion the revenue impact post-Revlimid and diversify growth levers going forward.

At the same time, Natco Pharma is planting seeds for future optionalities. Whether it’s their investment in eGenesis (pioneering genetically modified organ transplants) or NRC-2694 (a cell/gene therapy targeting late-stage head and neck cancer), it’s clear the company isn’t content playing the short game. They’re preparing for the next wave of innovation — and optionality.

Reasonable Valuations?

At just 9x PE and 6x EV/EBITDA, Natco Pharma is trading at the cheapest valuations in its history. Yet investors remain cautious. Why?

Because everyone’s asking: What happens after Revlimid?

That’s the elephant in the room.

If earnings drop (as expected) from ₹1,883 Cr to around ₹1300 Cr in FY26 as hinted by management the PE would not look cheap anymore — unless something fills the revenue void. Whether that’s semaglutide (India launch ~FY27), Risdiplam or a strategic acquisition, the key is execution.

But here’s where Natco stands out.

Despite the volatility, Natco Pharma has delivered industry-leading profit margins (nearly 50%), and ranks in the top 3 across 5- and 10-year sales and profit growth. Add a 5-year ROE of 18% — and this isn’t just a one-trick pony riding on Revlimid.

This is a company that’s played the boom-bust game before. Tamiflu in FY17. Revlimid in FY22. There was a dip each time. But they’ve come back stronger. And the fact that management has consistently “walked the talk” — building one pipeline while monetizing another — speaks volumes.

“You don’t make money by finding perfect companies. You make money when you find companies where the perception is worse than the reality.”

We believe most of the bad news is already in the price. The Revlimid cliff? Known. Near-term lumpiness? Expected. No immediate growth triggers? Already punished. What’s left now is a business with strong fundamentals, optionality in the pipeline, and a proven management team — trading at one of its cheapest valuations ever.