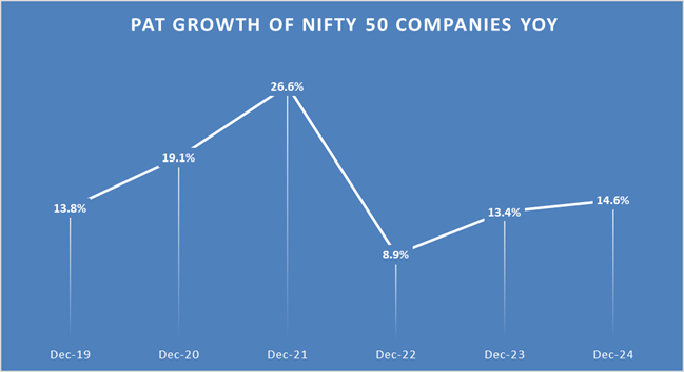

The recent 13% decline in the Nifty 50 index has been driven by stretched valuations, subdued Q3 earnings, concerns over Trump-era tariffs, and persistent FII outflows. With no new triggers to push stock prices higher, the market is undergoing a time correction, exacerbated by FII selling—This has led to panic selling often leaving retail investors bearing the brunt of these sell-offs.

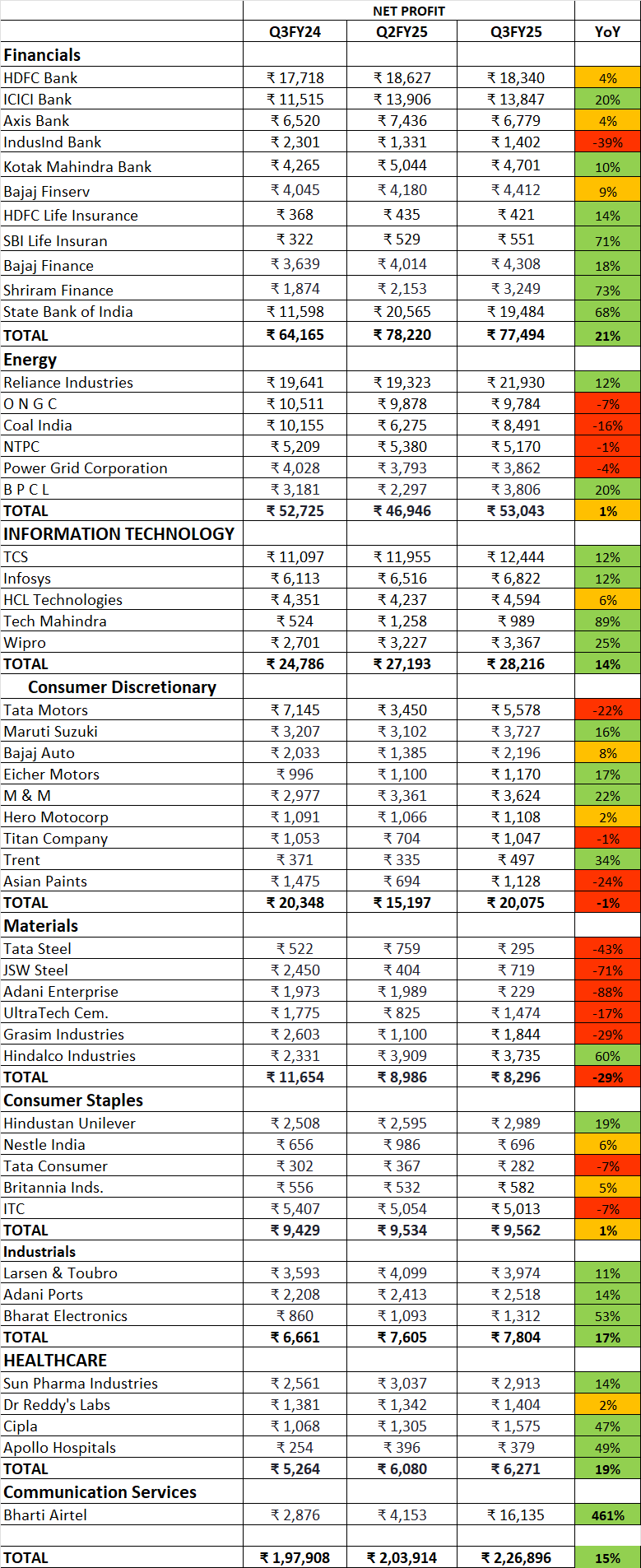

In Q3FY25, Nifty earnings grew ~15% YoY, significantly outpacing India’s GDP growth rate (~2.6x) and exceeding the previous two years’ earnings growth. Even on an adjusted basis, Nifty earnings demonstrated resilience, posting 9.3% YoY growth.

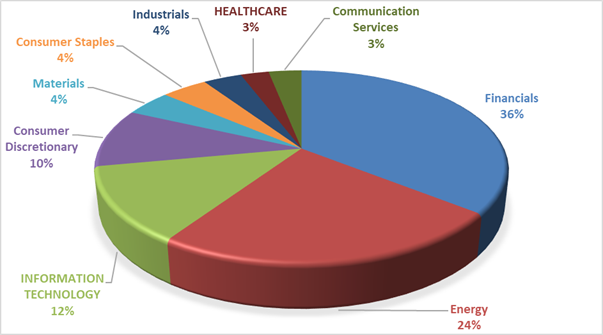

Earnings Growth Q3FY25 YOY

Sectoral Performance:

-

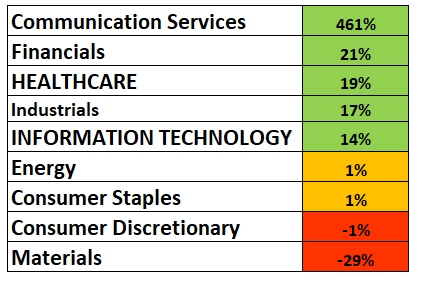

Top Performers:

- Communication Services (+461% YoY growth) contributing ~33% led the earnings surge, primarily driven by Bharti Airtel’s one-time exceptional gain of ₹7,546 crore from Indus Tower consolidation. However, adjusting for this, Airtel’s PAT still grew 121% YoY to ₹5,514 crore.

- Financials (+21% YoY growth) contributed ~7% to overall PAT growth, despite NIM compression from rising deposit costs and moderate loan growth.

- Healthcare, Industrials, and IT also supported earnings expansion.

-

Underperformers:

- Consumer Staples & Consumer Discretionary remained weak due to subdued private consumption demand.

- Materials & Energy were impacted by lower commodity prices (crude oil, coal), leading to weaker realizations.

What will drive Nifty earnings in coming Quarters?

Nifty 50 Companies Earnings Contribution Q3FY25

Four key sectors—Financials, Consumer Discretionary, Energy, and Information Technology—contribute approximately 82% to Nifty’s total earnings. For meaningful earnings growth, these sectors must expand at a pace exceeding GDP growth.

-

Energy & IT: Earnings in these sectors are largely influenced by global macroeconomic conditions. While IT continues to face profitability challenges due to slowdown in global markets, financials and consumer discretionary sectors require further impetus for sustained growth.

-

Macro Tailwinds: The Union Budget’s focus on boosting private demand, along with the RBI’s expected 50 bps rate cut and an accommodative policy stance, should provide strong support for economic expansion. Additionally, inflation has moderated to 4.25% in January 2025 (from 5.22% in December 2024), creating further room for policy intervention.

-

Sectoral Impact:

- Financials: Banks, which have faced NIM compression and rising deposit costs, will likely benefit from improved liquidity and strengthening credit demand.

- Consumer Staples & Discretionary: These sectors, which have underperformed in recent quarters, are poised for a recovery as both rural and urban demand show visible signs of revival.

With India’s GDP growth on track to reach 6.4% and Nifty earnings projected to grow 12% YoY in FY25, we anticipate a strong earnings revival in the coming quarters, led by financials and consumption-driven sectors.

0 Responses

What does one should do with Natco pharma? Down 40%