Sportking India Limited (Sportking), a leading yarn manufacturer, has delivered robust financial performance, efficient operations, and consistent growth. The company trades at a significant discount to peers with a P/E ratio of 12.3x compared to Ind PE of 18.75 and EV/EBITDA of 6x.

Its expanding margins, debt reduction efforts, and strategic initiatives such as moving up the value chain by forward integration highlight its growth potential, making it a compelling BUY opportunity.

- Revenue Growth: For FY25, management anticipates Revenues to be in the range of INR 2500 crores, plus or minus 5%, assuming no significant price fluctuations.

- Margins: Sportking aims to achieve EBITDA margins of 15%-17%, considered a reasonable target for a standalone spinning company.

- Export Markets: Stabilizing after disruptions, especially in Bangladesh. Global apparel demand recovery is a tailwind.

- Domestic Market: Supported by festive demand, rising discretionary spending, and government initiatives like PLI schemes.

- Capacity Expansion: Sportking is actively looking for opportunities to expand its spinning business, with potential announcements expected in the coming months. They are open to both brownfield and greenfield projects and are considering various geographic locations.

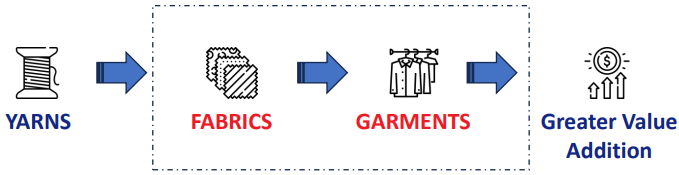

- Expanding into Higher-Margin Products: By moving into fabrics and garments through the merger, Sportking will be less reliant on the volatile yarn market and can tap into potentially higher-margin segments.

- Strategic Raw Material Management: Sportking covers its cotton needs for the next 6 months, providing a buffer against price fluctuations. Management believes cotton prices will remain stable in the next 3-4 years, further reducing this risk.

- Exploring New Markets: Sportking actively seeks new buyers and markets globally, reducing reliance on any single market. This approach helps mitigate risks associated with geopolitical uncertainties and regional economic slowdowns.

PROFIT & LOSS STATEMENT (Rs in Cr)

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24 |

| Revenue from Operation | 1355 | 1306 | 2154 | 2205 | 2377 |

| COGS | 1019 | 907 | 1288 | 1663 | 1860 |

| Gross Margin | 334 | 399 | 867 | 542 | 517 |

| Gross Margin % | 25 | 31 | 40 | 25 | 22 |

| Employee Cost | 89 | 87 | 116 | 116 | 139 |

| Other Expenses | 106 | 103 | 166 | 147 | 173 |

| EBITDA | 136 | 209 | 396 | 279 | 205 |

| EBITDA % | 10 | 16 | 18 | 13 | 9 |

| Depreciation and Amortisation Expense | 58 | 62 | 65 | 48 | 86 |

| Finance Costs | 52 | 54 | 29 | 29 | 59 |

| Other Income | 19 | 22 | 24 | 32 | 36 |

| PBT | 83 | 140 | 547 | 219 | 96 |

| PBT Margin % | 6 | 11 | 25 | 10 | 4 |

| Exceptional Items | 0 | 0 | 0 | 0 | 0 |

| Tax | 14 | 33 | 138 | 58 | 26 |

| PAT | 68 | 97 | 409 | 132 | 70 |

| PAT Margin % | 5 | 7 | 19 | 6 | 3 |

| Earnings per share (EPS) (Rs.) | 9 | 63 | 308 | 99 | 55 |

Margin Expansion Potential:

While recent years have seen a decline in profitability, Sportking’s management believes there is room for improvement and targets a 15%-17% EBITDA margin.

They are already seeing margin improvement through cost reduction efforts and a stable cotton price outlook contributes to their margin expansion goals., reaching 12% in Q2 FY25, and expect further increases as demand recovers.

This optimism is based on factors such as:

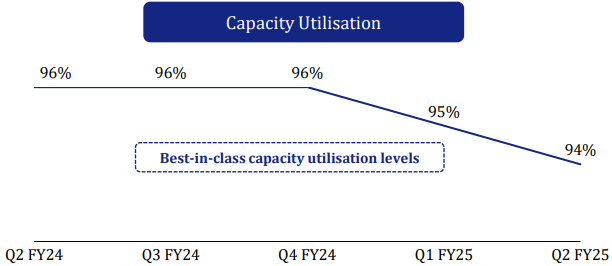

- Operational Efficiency: Sportking leverages large-scale production in Punjab with industry-leading utilization levels and consolidated operations.

- Cost Reduction Initiatives: The company targets a 100-basis-point cost reduction in six months through renewable energy investments and employee facility optimization.

- Solar Power Investment: A 40-megawatt solar plant investment aims to boost sustainability and improve EBITDA margins by 0.7%.

- Capacity Debottlenecking: Debottlenecking efforts are set to increase production volumes by 4%-6% from the next quarter.

- Favorable Raw Material Outlook: Stable cotton prices and six-month coverage reduce price volatility risks.

- Forward Integration: Merging Marvel Dyers, Processor Pvt Ltd, and Sobhagia Sales Pvt Ltd will extend operations across the textile value chain into fabrics and garments.

- Debt Management: Active repayment of short- and long-term borrowings strengthens the balance sheet.

Company Overview

Sportking is a prominent player in India’s textile industry, with a core focus on Yarn manufacturing (Cotton Yarn, Synthetic Yarn, Blended Yarn), Fabrics, and Garments.

Geographically, Sportking primarily operates in India, with its three state-of-the-art manufacturing facilities in Punjab. Sportking also exports to over 30 countries, with key markets including Bangladesh, Europe, and China.

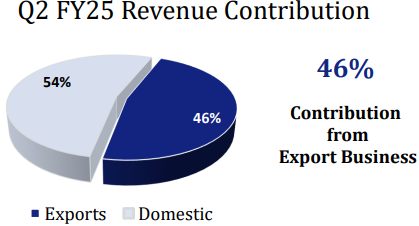

The company serves both domestic and export markets, maintaining a balanced revenue mix. Exports accounted for 46% of Q2 FY25 revenue, reflecting its strong global presence.

Key Strategic Update

Sportking has recently received approval for a merger with two companies: one specializes in Garment Dyeing and Finishing, while the other focuses on Garment Manufacturing. This proposed amalgamation will enable forward integration, allowing the company to manufacture and sell processed and dyed knitted fabric and garments. As a result, Sportking will offer a wider product range that caters to more customer needs. Additionally, this integration aims to achieve higher profit margins by capturing value across the entire textile value chain.

MARQUEE CUSTOMERS

Sportking’s Competitive Positioning (Moat) Analysis

Scale: Sportking benefits from economies of scale due to its large production capacity. With a total spindle count of 379,000, Sportking can produce yarns at a lower cost per unit compared to smaller competitors.

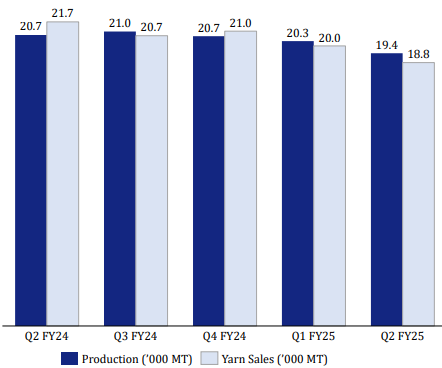

Sportking also has one of the best utilization levels in the industry, indicating efficient use of its capacity. This efficient operation at scale is highlighted as one of Sportking’s key strengths.

This high utilization rate indicates efficient operations and consistent outperformance, as selling more than what it produces reflects a strong demand for Sportking’s yarn products.

Reputation for Premium Quality: Sportking’s consistent focus on delivering high-quality yarns has earned it recognition among discerning global garment brands.

Customer-Centric Approach: Their responsiveness to market trends and customer needs, competitive pricing, and prompt service strengthens customer relationships and fosters loyalty.

Industry Analysis

Sector Dynamics

India’s textile industry is consolidating, with inefficient players exiting due to high costs and low competitiveness. Efficient firms like Sportking stand to gain market share and profitability as the sector recovers.

- India’s textiles sector is at an inflection point – The sector can act fast and grab the huge opportunity to open up due to a change in global textile trade patterns. While the opportunity is huge, the government and the industry need to act in coordination, and fast, as the world will not wait.

- India is emerging as a powerhouse in exports- Currently textile sector exports stand at $34.43bn at the end of FY24, which is expected to breach $100bn by the end of FY30.

- China +1 strategy- A lot of developed countries are moving their suppliers from China to other major textile countries, India being the second largest cotton producer, is going to have a massive opportunity from this strategy utilized by developed countries like USA and EU.

Key Risks

- Raw Material Dependency: Cotton price volatility could pressure margins.

- Demand Uncertainty: Slower recovery in export or domestic markets may hinder growth.

- Geopolitical Risks: Export markets remain vulnerable to trade tensions or policy changes.

- Cotton Price Volatility: Higher Minimum Support Prices (MSP) in India could impact competitiveness.

- Freight Costs: Global shipping disruptions remain a potential risk.

0 Responses

This company also depends on the Bangladesh yarn exports . Bangladesh is a major buyer of Indian yarn

They need to move towards integration to improve margins