Spotting Market Mispricing: After Natco, We Turn to Tata Motors

Markets make mistakes. And they usually don’t make them everywhere — they show up in pockets.

If you’re not actively looking, you’ll miss them.

Sometimes, the mispricing is obvious — like watching a fundamentally sound business punished for near-term volatility. Other times, it requires digging deep, challenging consensus narratives, and doing the kind of work most people avoid.

We highlighted one such opportunity earlier with Natco Pharma, where the market seemed to be overly focused on the “Revlimid cliff” and completely ignored a deep, optionality-filled pipeline. That stock was beaten down for all the wrong reasons — despite strong margins, future-facing bets, and one of the most attractive valuations in the entire pharma space.

You can read that full breakdown [Natco Pharma – Betting on the Jockey].

But today, we’re turning our attention to a very different sector — Autos.

And a company that’s quietly transforming its business in a way the market still hasn’t fully priced in.

Let’s talk about Tata Motors.

Tata Motors sits at the heart of India’s EV revolution—commanding ~55% market share in the fastest-growing electric vehicle market on the planet.

And yet, despite this dominance, a robust and expanding EV ecosystem, a $130 billion market opportunity by 2030, $15+ billion worth of value unlocking through strategic moves, and JLR posting record profits—the stock trades at just 8.97x PE.

That’s a massive 247% discount to Indian auto peers.

Maruti Suzuki, largely absent from the EV space, commands 27x PE. Meanwhile, global EV leaders like Tesla trade at 168.8x forward PE and BYD at 18.4x PE, despite Tata Motors’ stronger competitive position in the world’s third-largest automotive market

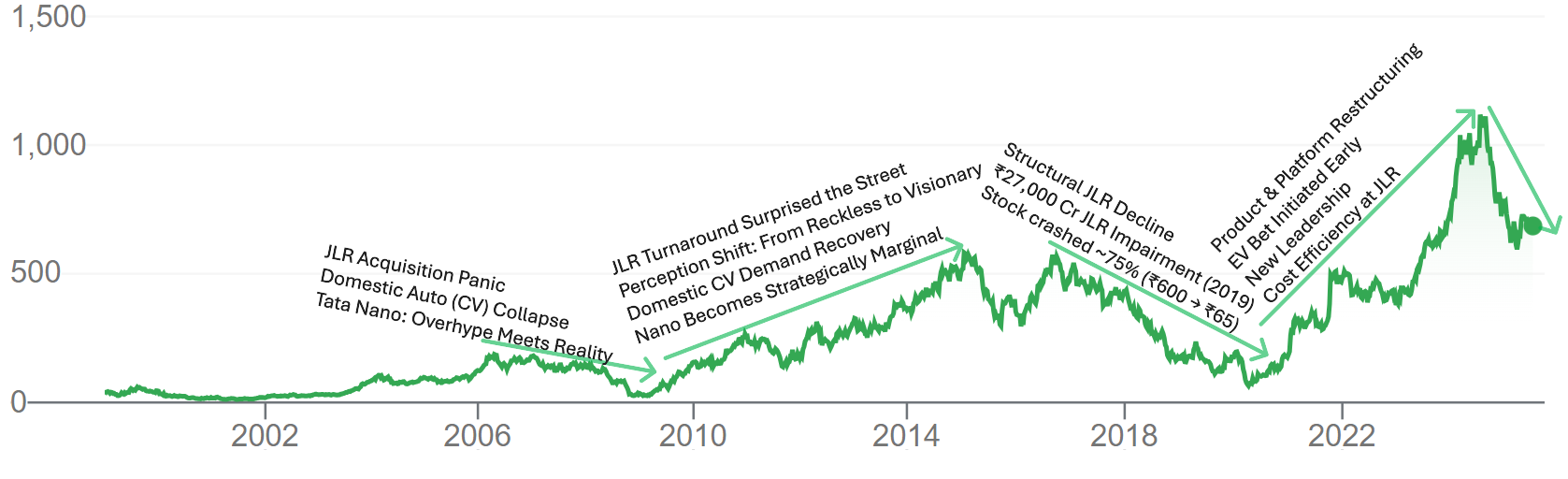

Historical Precedent: Why the Market Gets Tata Wrong

While markets often obsess over near-term triggers—be it a quarterly miss, margin pressure, or order flow—the long arc of Tata Motors tells a different story.

From the panic around the JLR acquisition to its stunning turnaround, from the overhyped Nano to strategic clarity, and from a ₹27,000 Cr JLR impairment to a bold EV pivot—Tata Motors has repeatedly played a longer game that the market caught on to only in hindsight.

Current Parallel: Similar skepticism exists today regarding the EV transformation, despite far stronger fundamentals including dominant market share, government support, and technological advantages. ~(Discussed below)

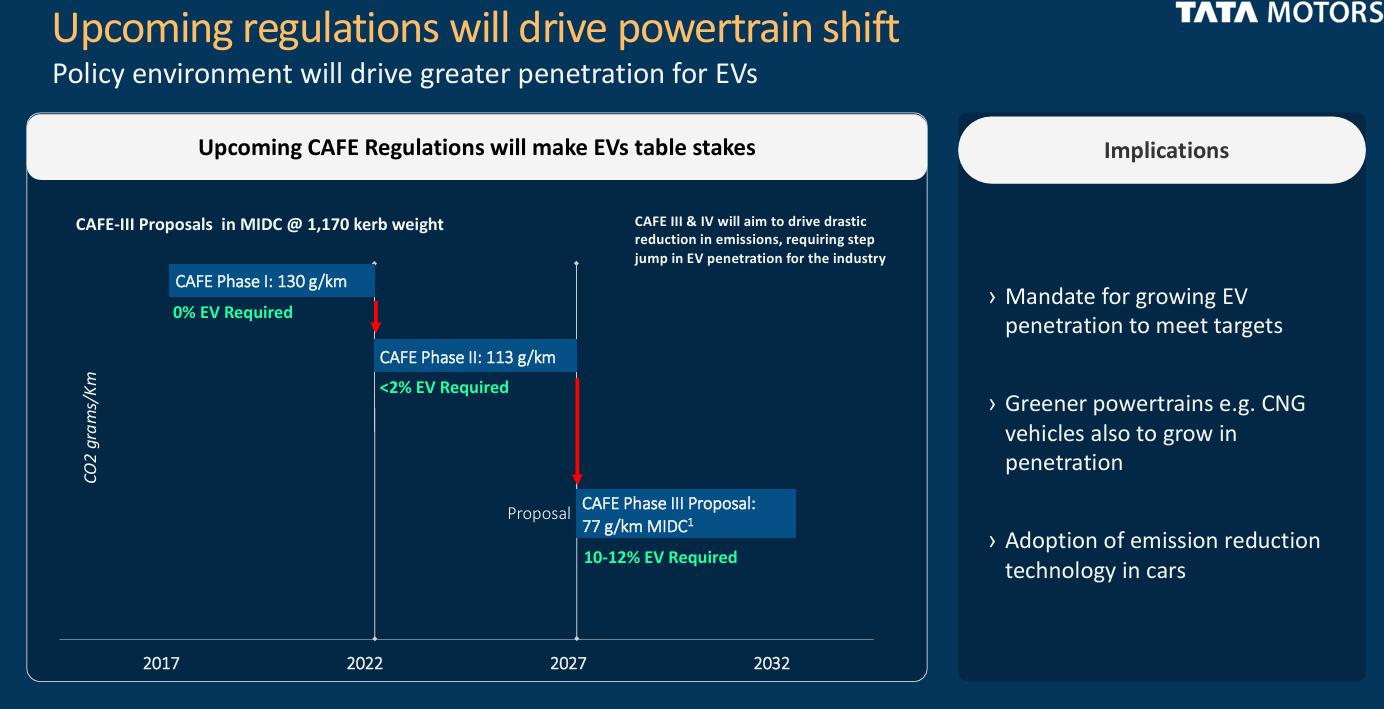

What gives us the confidence that EVs are here to stay despite all the noise and uncertainty?

This slide from Tata Motors makes it crystal clear: upcoming CAFE-III and CAFE-IV regulations are tightening carbon emission norms sharply (from 130 g/km → 113 g/km → proposed 77 g/km by 2027). To meet these, the industry will be mandated to ensure 10–12% EV penetration—EVs will no longer be optional; they’ll be essential.

Looking Beyond the Numbers: Where the Real Value Hides

Markets often obsess over quarterly figures—EBIT margins, free cash flows, volume growth. But real, sustainable value often emerges from what happens long before those numbers show up.

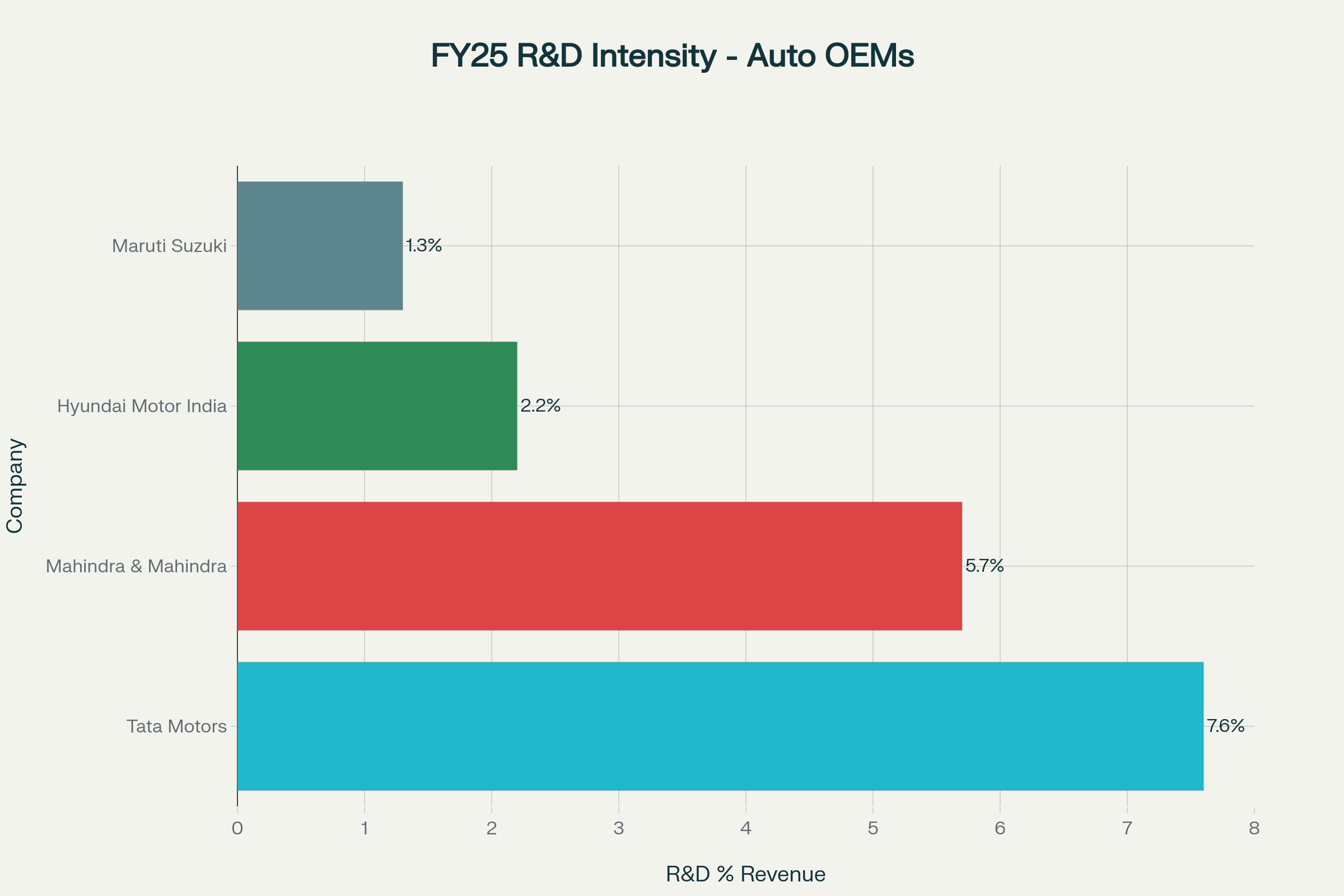

R&D is that early engine.

Why it matters

-

High R&D intensity is correlated with faster product cycles and tech ownership—critical in the shift to EVs.

-

In FY25 Tata filed a record 250 patents and 148 industrial designs, underscoring both volume and quality of innovation

-

India’s R&D Leader

Tata Motors reinvested ~7.6% of FY25 revenue into R&D—over 3× Maruti and well above Mahindra. -

Competing with Global Giants

Tata’s consolidated $4B R&D spend now on par with global EV pure-plays, despite a much smaller revenue base. JLR alone accounts for £3.8B, supplying Tata’s next-gen EV platforms like EMA. -

Tech Driving Market Share & Margins

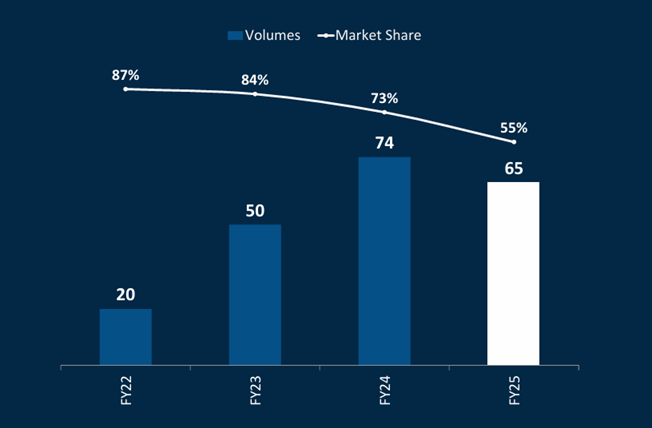

Even after EV share dropped from 87% to 55%, Tata still outsold its next three competitors combined. Critically, EV EBITDA margin flipped positive (+1.2%) in FY25—a rarity among global mass-market EV players.

EV Numbers Don’t Lie: Behind Tata’s Revenue Mix

Let’s start with what the Street thinks it knows: Tata Motors is largely a traditional auto company.

-

FY25 Total Revenue: ₹4.39 lakh crore

-

EV Revenue: ₹8,187 crore

-

EV Share of Total Revenue: Just 1.86%

- Slowing EV Growth Market share eroded from 87% to ~55%

On the surface, EVs barely move the needle. But this is a classic case of the iceberg illusion—what’s visible is only a sliver of the full story.

Here’s what you’re missing:

-

Tata’s EV revenue is ~16.9% of its Passenger Vehicle business

-

The EV business turned EBITDA-positive in FY25 (+1.2%), despite a volume decline and subsidy headwinds

-

Tata still holds 55% of India’s EV market, despite competition from Mahindra, Hyundai, and new entrants

The upcoming demerger is the real catalyst that will finally make the EV narrative visible. Today, Tata’s EV business appears small (~2% of total revenue) because it sits inside a large, consolidated auto structure that includes commercial vehicles, legacy operations, and JLR—all mashed into one.

Post-demerger in FY26, the picture changes. The Passenger Vehicle + EV + JLR entity (to be renamed Tata Motors Passenger Vehicles Limited) will stand independently—and the EV business will be seen in its true context: as a key growth engine within a sharply focused PV/EV powerhouse.

Add to that the JLR EV transformation story, and you get a two-pronged growth engine: mass-market EV dominance at home, and luxury EV optionality abroad.

The real value is not in the percentage of EV revenue today, but in the infrastructure, ecosystem, and future cash flows being built underneath.

The Dominant Mass Market EV Player, by Miles

Here’s how Tata stacks up against its peers in FY25:

| OEM | EV Sales (Units) | Market Share (%) | Launch Status |

|---|---|---|---|

| Tata Motors | 57,616 | 55% | Full lineup from entry to premium |

| Mahindra | 8,182 | ~7.6% | Focus on SUVs, limited portfolio |

| Hyundai | 2,410 | ~2.2% | Creta EV coming Q4 FY25 |

| Maruti Suzuki | 0 | 0% | e-Vitara coming in FY26 |

Tata Motors’ EV Play: It’s Not Just Ahead—It’s Playing a Different Game

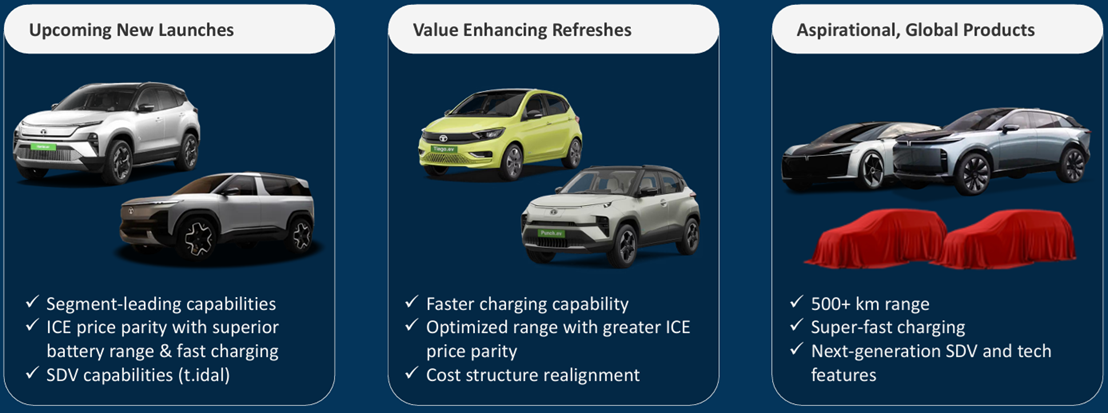

Tata’s early EV success came from dominating the entry-level space. But that left gaps—especially in the ₹12–20 lakh mid-segment and the premium ₹20 lakh+ category, where rivals launched flashier, tech-loaded models.

While the market saw Tata as lagging, it was quietly setting up a smarter strategy: a “two-products-per-segment” approach—Tiago & Tigor EVs at entry-level, Altroz, Punch & Nexon EVs in the mid-range, and now Curvv, Harrier & Safari EVs at the premium end.

Instead of chasing headlines, Tata is building depth and defending its EV market share. And from 2026, it’s going premium with next-gen Avinya and Sierra EVs

The Ziptron Technology Stack

Tata Motors’ Ziptron platform is the result of nearly a decade of in-house EV innovation. It powers Tata’s EVs with strong range, top-tier safety, and smooth performance. Unlike rivals that depend on imported parts, Tata’s homegrown tech brings down costs and speeds up product development.

While other OEMs are navigating the EV transition cautiously, Tata’s EV arm is already profitable:

-

EV EBITDA Margin FY24: –7.1%

-

EV EBITDA Margin FY25: +1.2%

Even with a 10% decline in EV volumes (due to subsidy expiration), Tata’s margin jumped 8.3 percentage points

Looking ahead, the upcoming Gen 3 EVs—built on JLR’s advanced EMA platform—promise world-class efficiency and L2+ autonomous driving features, setting the stage for Tata’s next leap in EV leadership.

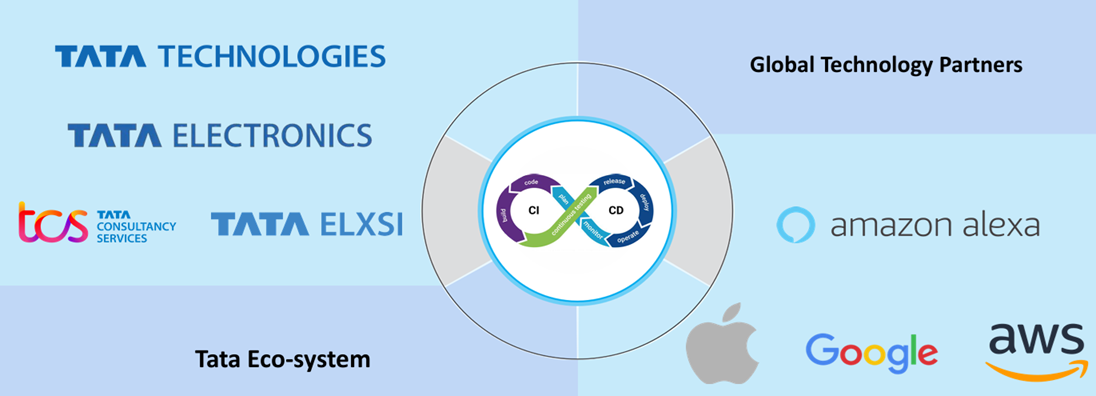

The “One Tata” Flywheel: A Meta-Style Moat

No other OEM in India can match the synergistic loop Tata has created across its group companies:

| Domain | Tata Group Arm | Strategic Advantage |

|---|---|---|

| Charging | Tata Power | Largest EV charging network in India |

| Battery & Components | Agratas, Tata AutoComp | Local cell-to-pack manufacturing, BMS integration |

| Software & Connectivity | Tata Elxsi, TCS | SDV stack, OTA, V2G, AI diagnostics |

| Finance & Loyalty | Tata Capital, Tata Neu | Fintech tie-ins, personalized offers, loyalty flywheel |

JLR: Tata Motors’ Premium EV Growth Engine

Jaguar Land Rover (JLR), which still accounts for ~70% of Tata Motors’ consolidated revenues, recently cut its FY26 guidance—flagging a dip in EBIT margins to 5–7% (from 8.5% in FY25) and “near-zero” free cash flow.

This announcement triggered a 5% stock drop in June 2025 and continues to cast a shadow on Tata Motors’ valuation.

But the Market Is Missing the Bigger Picture

While investors are fixated on near-term margin pressures, JLR is laying the foundation for its next leg of profitable, EV-driven growth:

1. EMA Licensing – Born-EV Advantage

-

Tata’s EV arm (TPEM) licensed JLR’s Electrified Modular Architecture (EMA) for the Avinya series (July 2025).

-

Moat: EMA offers native BEV design, advanced electronics, L2+ ADAS, OTA software, and cell-to-pack battery integration—outclasses mass-market EV platforms globally.

2. Premium Positioning – “House of Brands”

-

JLR targets full-electric Jaguar line-up by 2025 and Land Rover by 2030 under its Reimagine plan.

-

Moat: Luxury icons (Range Rover, Jaguar, Defender) deliver high ASPs, customer stickiness, and brand equity in a 20–25% CAGR segment.

3. Global R&D & India Manufacturing Synergies

-

Sanand plant to build both TPEM’s Gen 3 and export-bound JLR EVs using localized EMA and Agratas battery packs.

-

£15B EV investment includes Halewood conversion and e-propulsion unit facility in the UK.

-

Moat: Shared R&D and manufacturing drive cost leadership and buffer supply/policy shocks—an antifragile cost model.

4. Luxury Margins & Diversified Optionality

-

JLR’s EVs to deliver ASPs of $100K+, 700 km range, and 10–15% EBIT margins.

-

Moat: Premium EVs sidestep price wars, target a rich, underpenetrated global luxury EV market (EU, US, China).

5. Integrated Software + Ecosystem Flywheel

-

Advanced features: OTA updates, digital cockpit, Tata Elxsi integration, and Tata Neu-backed personalization.

-

Moat: A software-defined luxury experience that’s hard to replicate—boosts user lock-in and monetization.

6. Dual-Engine Optionality vs. Global Peers

-

Unlike Tesla’s single brand, Tata has dual play: mass-market EVs (TPEM) + luxury EVs (JLR).

-

Moat: Geographic and brand diversification reduces risk and maximizes growth capture across segments.

Demerger Optionality: JLR EVs as standalone entity could fetch 20–25x EV/EBITDA, unlocking value.

Investor Takeaway: Look Again

If you’re valuing Tata Motors like an auto stock, you’re missing the real story.

Tata isn’t just building cars—it’s creating the rails on which India’s EV economy will run. With deep vertical integration, software-driven evolution, and unmatched infrastructure.