Unless you’re living under a rock or you’re a total novice to the investing community, you would have heard about the Hot IPO of WAAREE ENERGIES ~Fun Fact Waaree Energies IPO broke the record by receiving the highest number of applications for an IPO at 97.34 lakh.

The Rs 4321 Crore IPO was oversubscribed 76.34 times which means people threw in Rs 333000 Crore trying to get a piece of Rs 4321 Crore.

Now if you Missed out on this dream IPO? You’re not alone! But don’t worry—this report is crafted to give you the insights you need to make informed decisions if you’re still eager to invest in this exciting company.

Reasons to Consider Investing in Waaree Energies

The Big Question is why should we consider going solar?

With a population of 1.4 billion, India has a massive demand for energy to fuel its rapidly growing economy. From a power-deficient nation at the time of Independence, efforts to make India energy-independent have continued for over seven decades.

Reason 1 – Energy Security and Independence: India imports over 80% of its oil needs, making it vulnerable to global price fluctuations and geopolitical tensions.

- Renewable energy offers a path to reduce this dependence. For instance, India’s solar capacity growth to 85 GW in 2023 has already started reducing fossil fuel imports.

Reason 2—As the world grapples with the urgent need to combat climate change, India has set a target to reduce the nation’s economy’s carbon intensity by less than 45% by the end of the decade, achieve 50 percent cumulative electric power installed by 2030 from renewables, and achieve net-zero carbon emissions by 2070. India aims for 500 GW of renewable energy installed capacity by 2030.

INDIA ENERGY BASKET

| TOTAL INSTALLED CAPACITY – 453 GW | ||

| TOTAL RENEWABLE INSTALLED CAPACITY – 210 GW | ||

| TOTAL RENEWABLE INSTALLED CAPACITY IN (%) TERMS ~ 46% | ||

| Year | Source | Installed Capacity (in GW) |

| 2024-25 | Coal | 217.59 |

| 2024-25 | Oil & Gas | 25.41 |

| 2024-25 | Solar | 90.76 |

| 2024-25 | Wind | 47.36 |

| 2024-25 | Small Hydro | 5.07 |

| 2024-25 | Large Hydro | 46.93 |

| 2024-25 | Waste to Energy | 0.6 |

| 2024-25 | Nuclear | 8.18 |

| 2024-25 | Biomass/Co-generation | 11.33 |

| Total | 453.23 | |

As shown in the data, India’s installed power generation capacity has been on a consistent upward trend, with solar energy leading this growth trajectory. To meet the Net Zero Emissions Scenario by 2050, India needs its generation capacity to grow by an average of 25% each year from 2022 to 2030. This ambitious target translates to more than a threefold increase in annual capacity deployment over the next decade.

CRISIL Consulting estimates that between FY2024 and FY2028, India will add approximately 130-140 GW of solar capacity, alongside 24-25 GW from wind. This projected surge in capacity demonstrates the favorable outlook for solar companies, with Waree Energies positioned at the forefront of this growth wave.

With solar becoming the preferred, lowest-cost option for electricity generation globally, investments in solar PV are expected to accelerate. Among India’s commercially viable renewable sources, solar holds the greatest potential, providing a strong foundation for Waaree Energies to capitalize on these market dynamics and establish its leadership in the sector.

Where else can you find a company with such tremendous growth potential and strong industry tailwinds that even a 2x or 3x increase in revenues might still fall short of meeting the full market demand?

Waree Energies stands as India’s largest solar PV module manufacturer, boasting an impressive installed capacity of 12 GW. Founded in 2007 with a focus on delivering quality, cost-effective solar solutions, the company has evolved into a leader in sustainable energy. Rapidly expanding from 2 GW in FY2021 to 9 GW by March 2023, and reaching 12 GW by June.

Waaree’s pending order book for solar PV modules stands at 20.16 GW, including domestic, export, and franchisee orders, with an additional 3.75 GW, prompting the company to build significant capacity

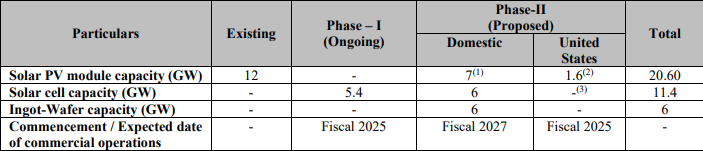

To meet this demand the company plans to expand its solar PV module capacity from 12 GW to 20.6 GW, adding 8.6 GW through ongoing and proposed projects in both domestic and U.S. markets, with expected commercial operations beginning between fiscal 2025 and 2027.

Margin Expansion Through Backward Integration

In addition to its capacity expansion, the company is pursuing backward integration by adding 6 GW of ingot-wafer capacity and 6 GW of solar cell capacity, key raw materials in the solar PV module value chain. This strategic move is expected to enhance operational efficiencies and improve profit margins.

To tap customers in the United States and globally, the company is establishing a 1.6 GW solar PV module manufacturing facility in Houston, Texas in the United States which is expected to be operational by the end of Fiscal 2025 which can be further expanded by an additional 1.4 GW subject to market conditions to a total of 3 GW installed capacity by Fiscal 2026 and 5 GW of solar module manufacturing facility by Fiscal 2027.

What Does The Waaree Energies DO

Waaree manufactures solar PV modules using multi-crystalline and monocrystalline cell technologies, as well as advanced technologies like Tunnel Oxide Passivated Contact (TopCon), which help reduce energy loss and improve overall efficiency.

The company has a pan-India retail network consisting of franchisees. As of March 31, 2021, 2022 and 2023 and as of

June 30, 2023, retail network consisted of 290, 373, 253 and 284 franchisees across India, respectively.

The overall portfolio of solar energy products consists of the following

PV modules: (i) multicrystalline modules; (ii) monocrystalline modules; and (iii) TopCon modules, comprising flexible modules, which include bifacial modules (Mono PERC) (framed and unframed), and building integrated photo voltaic (BIPV) modules.

The company operates across four manufacturing facilities in India, covering a total area of 136.30 acres. These facilities are located in Gujarat, with one factory each in Surat (“Surat Facility”), Tumb (“Tumb Facility”), Nandigram (“Nandigram Facility”), and Chikhli (“Chikhli Facility”).

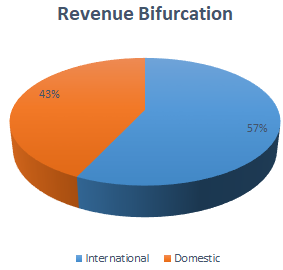

Revenue Bifurcation

Increasing global demand for solar capacity, coupled with international policies like China plus 1 and anti-dumping duties on Chinese solar products, has resulted in rising export sales, boosting revenue and margins. The “China Plus One” strategy is further promoting solar manufacturing in regions like India, and Waaree energies will be the biggest beneficiary of such policies

Now, we arrive at the most exciting part of the report: The numbers.

| Mar-20 | Mar-21 | Mar-22 | Mar-23 | Mar-24 | |

| Sales | 1,996 | 1,953 | 2,854 | 6,751 | 11,398 |

| Expenses | 1,903 | 1,868 | 2,748 | 5,915 | 9,823 |

| Operating Profit | 93 | 85 | 106 | 836 | 1,575 |

| OPM % | 5% | 4% | 4% | 12% | 14% |

| Other Income | 25 | 45 | 97 | 88 | 576 |

| Interest | 34 | 30 | 41 | 82 | 140 |

| Depreciation | 27 | 29 | 43 | 164 | 277 |

| Profit before tax | 57 | 71 | 118 | 677 | 1,734 |

| Tax % | 31% | 33% | 33% | 26% | 27% |

| Net Profit | 39 | 48 | 80 | 500 | 1,274 |

| EPS in Rs | 2.12 | 2.46 | 3.84 | 24.49 | 62.76 |

| ROCE | 43.60% | ||||

| ROE | 33.40% |

Robust Revenue and Profit Growth

Waaree’s revenue grew at a remarkable 54% CAGR from ₹1,996 crore in FY20 to ₹11,398 crore in FY24. Net profit soared by 107% CAGR, highlighting strong demand and successful market expansion.

Expanding Margins and Operating Leverage

Operating profit margin improved from 5% in FY20 to 14% in FY24, reflecting Waaree’s enhanced cost efficiency and economies of scale. Advanced technologies like TopCon further support margin growth.

Strong Return on Equity and Capital Employed

In FY24, Waaree achieved an impressive ROCE of 43.6% and ROE of 33.4%, demonstrating efficient capital utilization and robust profitability. These returns highlight the success of its growth strategy.

Strategic Backward Integration to Support Margin Expansion

Backward integration into ingot-wafer and solar cell production reduces supply chain dependencies and enhances margins. This vertical integration strengthens Waaree’s cost structure and market competitiveness.

Excellent 👍👌

Compilation with facts and marketing trend.

Excellent analysis done with full clarity.

Good

Knowledgeable article and detailed one.

Very good analysis

Thanks

Excellent analysis and recommendations. I am very bullish on Waree Energies along with Insolation energy and premier energy but Waree will win the war and will outperform

Job requirement for an Asst. Mgr. Product Development and Marketing Engineer.

Barun Kumar Das

Mobile : 70035 20801

Good information boss … Thank you…

Hi,

Thanks for detailed article. Can you please also add following points.

1. What is cost structure vs china

2. What will happen if govt stops protecting from cheap china imports.

WAAREEENER is vv cost Saving & one of the Best cost Saving company in the Whole World.

At what price should I sell this share

waree energy suoerb

I intersected solar business for waaree energies opportunities, please contact me. I am from Vidisha MP postcode 464001, name, Ayush Chouksey

Sir plzzz contact me 9340973029