India wants to increase the share of natural gas in its energy mix. That means the country needs more LNG terminals, more pipelines, more CNG stations, more PNG connections, and more city gas networks.

So the gas value chain has a long runway.

When it comes to gas, many investors make the mistake of treating the entire sector as one basket.

That is a mistake.

Gas is not one business. It is a chain of very different businesses, each with a different economic engine, different risk profile, different pricing power, and different valuation logic.

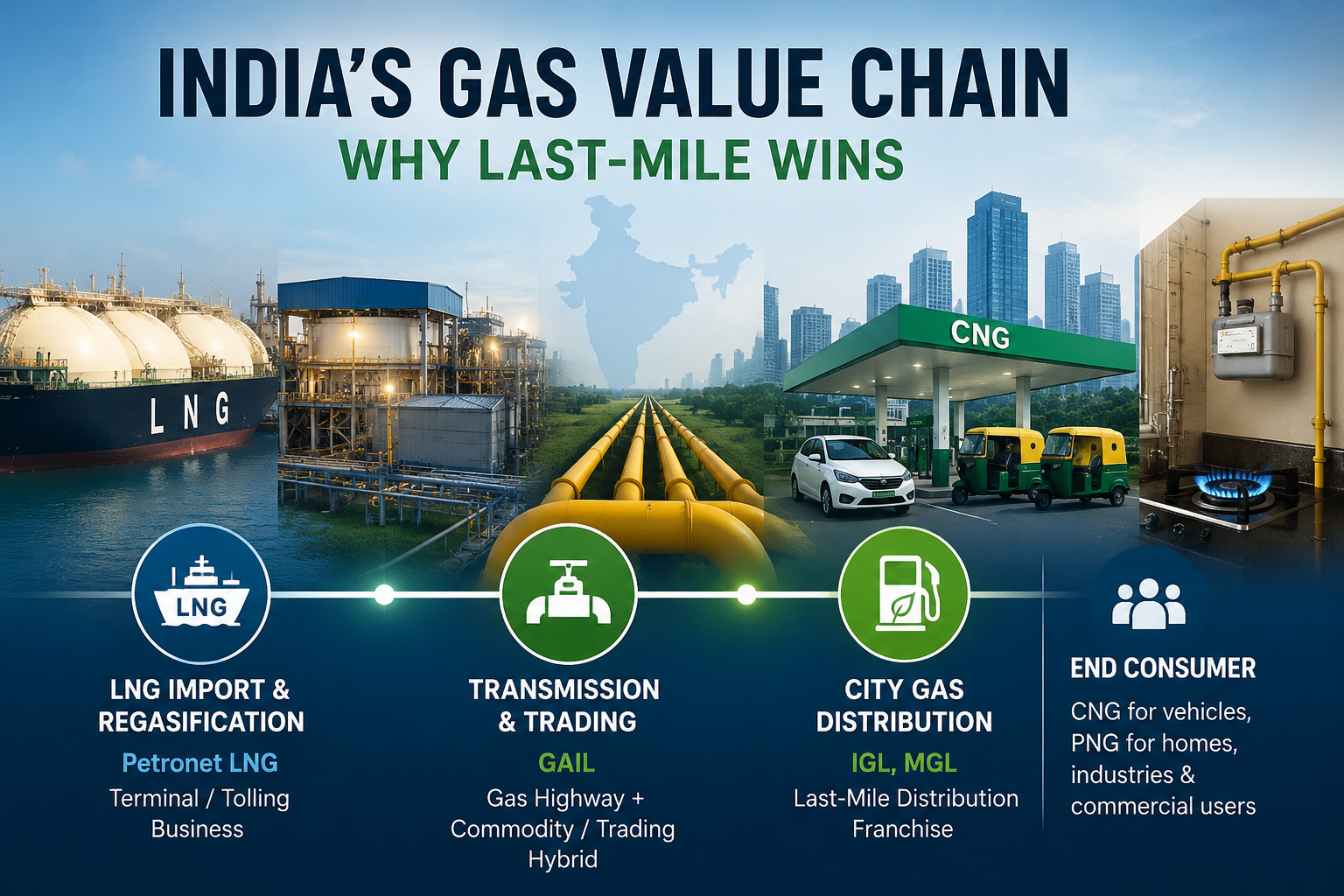

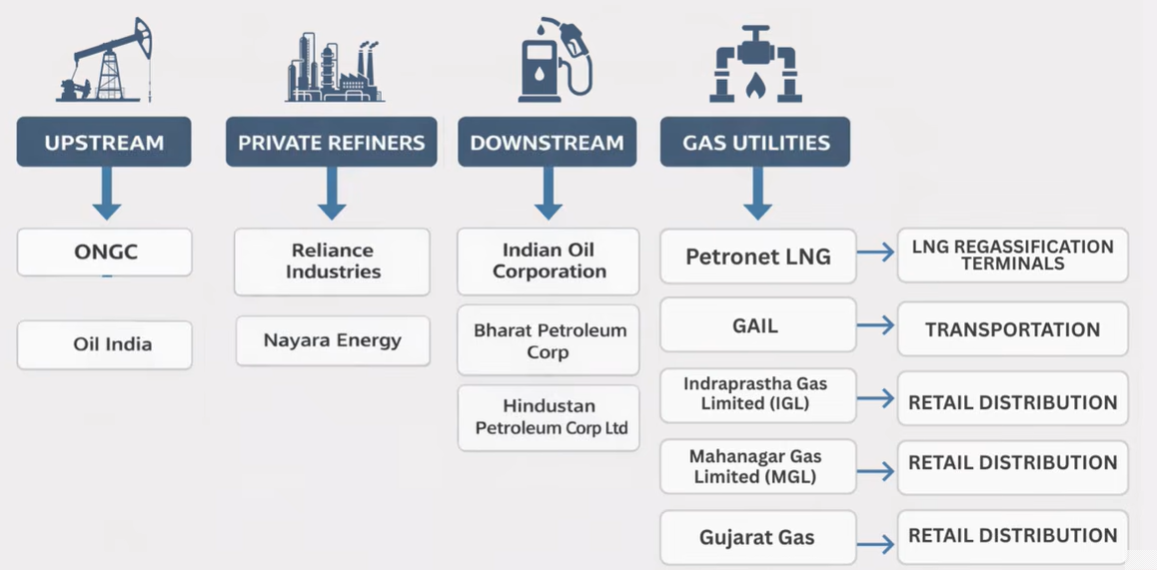

Broadly, India’s gas value chain can be divided into three layers:

| Segment | Representative Companies | What They Do | Economic Character |

|---|---|---|---|

| LNG import and regasification | Petronet LNG | Import LNG, store it, regasify it, and send it into the gas grid | Terminal/tolling business |

| Transmission and trading | GAIL | Owns pipelines, transports gas, trades gas, participates in LNG and downstream businesses | Gas highway + commodity/trading hybrid |

| City gas distribution | IGL, MGL | Sell CNG to vehicles and PNG to households/industries | Last-mile distribution franchise |

The closer a company is to the end customer, the more interesting its economics can become – provided the business has network density, local exclusivity, and reasonable ability to pass through costs.

That is why the most interesting part of the gas value chain, in our view, is not necessarily the LNG terminal or the national pipeline. It is the city gas distribution business — companies like IGL and MGL.

City Gas Distribution: Why IGL and MGL Are the Most Interesting Gas Businesses

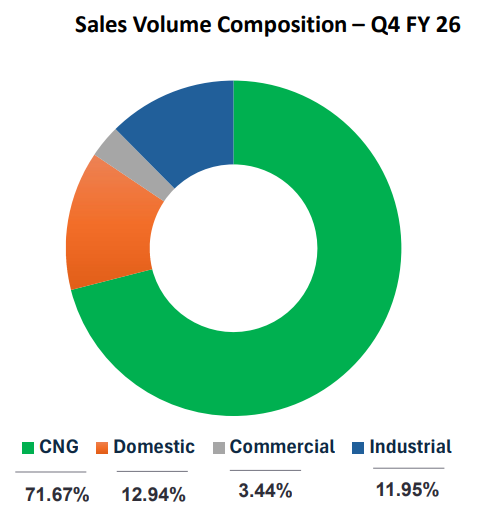

MGL Sales Volume Composition

IGL and MGL earn most of their revenue from CNG sold to vehicles through CNG stations. The balance comes from PNG supplied to homes, commercial users and industries.

This is why CGD is the most interesting part of the chain. Petronet and GAIL serve large institutional buyers; IGL and MGL serve the end customer.

That difference matters.

A dense CNG and PNG network creates local stickiness. More stations improve convenience. More household connections improve stability. More industrial users improve scale.

So the business is not just selling gas. It is building a local utility network.

That is why, in our view, IGL and MGL have better long-term economics than the upstream parts of the gas chain.

Petronet LNG: Throughput, Not LNG Price

Petronet LNG is not a direct bet on LNG prices. It is a regasification business.

It imports LNG, stores it, converts it back into gas and earns a regasification charge. So the key driver is not LNG price, but volume.

If LNG availability or demand falls, Petronet processes less gas and earnings suffer. If volumes rise, profitability improves.

The limitation is pricing power. Petronet’s customers are largely large PSU/institutional buyers, and tariffs remain policy-sensitive.

So while Petronet owns critical infrastructure, it is not the most attractive part of the gas value chain.

The Opportunity: Margin Pain in IGL and MGL

IGL and MGL have better economics because they sell directly to end customers. The government does not directly cap their CNG/PNG selling price, but it can still affect margins indirectly through APM gas allocation.

If cheaper domestic gas allocation is reduced, or the allotted gas becomes costlier, their raw material cost rises. They cannot pass this on aggressively because CNG must remain cheaper than petrol, diesel and EV alternatives. So margins take a hit.

That is the current problem.

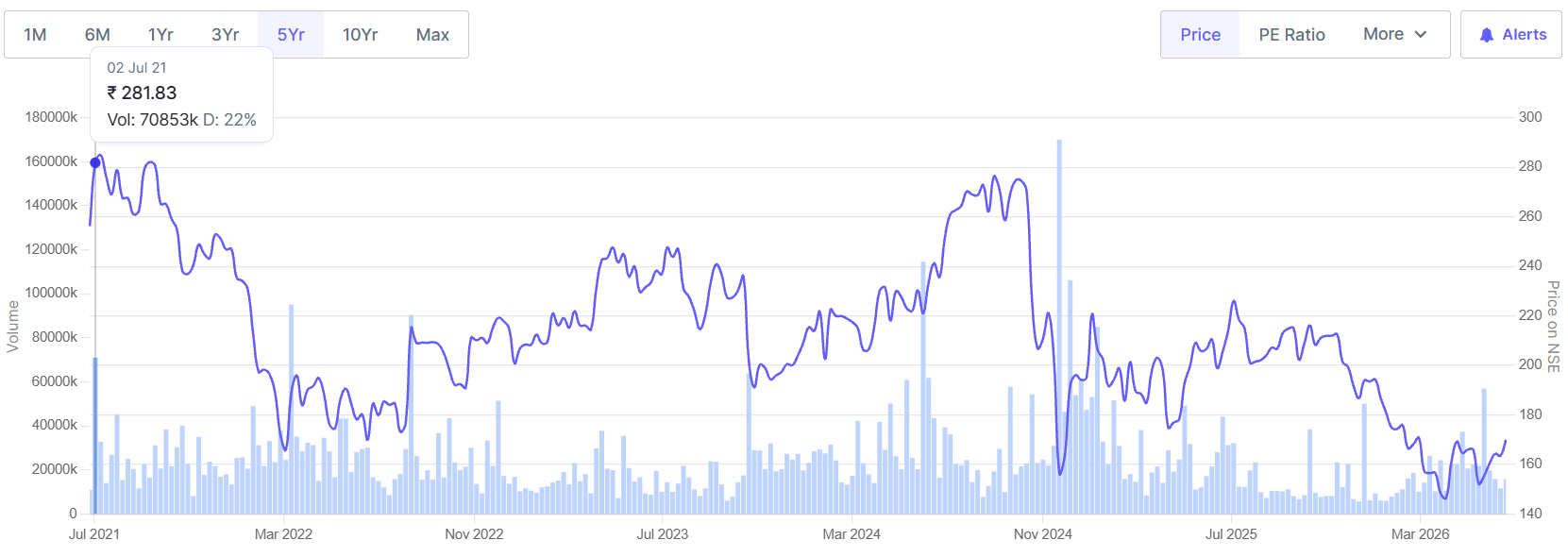

IGL 5yr Price Chart

But this is also why the opportunity exists. Stocks like IGL have corrected sharply — from around ₹281 earlier to nearly ₹146 at one point — and now offer around 2.5% dividend yield. Still, this is not a dividend story. It is a long-term growth story.

India wants cleaner fuel, lower pollution and lower crude import dependence. Gas is partly domestically produced, and pipeline expansion remains a policy priority. Even if EVs grow in passenger and commercial vehicles, gas still has a role in households, kitchens, industries and fertilizer plants.

So with a 10-year view, IGL and MGL remain the more attractive last-mile gas franchises.

Final Take

The reason we like this space is simple: gas has a long-term growth runway in India.

The government wants cleaner fuel, lower pollution and lower dependence on imported crude. That keeps pipeline expansion, CNG adoption and PNG penetration structurally relevant.

This is where GAIL benefits as the gas pipeline backbone of the country. But the more attractive business construct, in our view, is still retail distribution through IGL and MGL.

They are available at much cheaper valuations than before, while the long-term opportunity remains intact. Even if EV adoption grows in vehicles, gas still has a large role in households, kitchens, and industries.

So with a 10-year view, GAIL is a good infrastructure play, but IGL and MGL remain the more interesting last-mile gas franchises.