Incorporated in 2015, Freshara Agro Exports Ltd is a producer and exporter of preserved gherkins and related products, Freshara specializes in procurement, processing, and exporting preserved gherkins and pickled vegetables. Its products are certified by FSSAI, FDA, Star-K Kosher, APEDA, IFS, and BRCGS, meeting international quality standards

The “local” Arbitrage

Industry Analysis: The Global Pickle Economy

To understand Freshara’s potential, one must understand the global dynamics of the pickled vegetable industry—a niche but highly resilient segment of the processed food market.

Global Gherkin Market Dynamics

The global market for pickled cucumbers and gherkins is projected to grow from USD 1.58 Billion in 2025 to USD 1.96 Billion by 2030, registering a CAGR of 4.4%. However, the traded market is shifting geographically, with production moving away from high-cost regions (Europe, US) to low-cost agrarian economies.

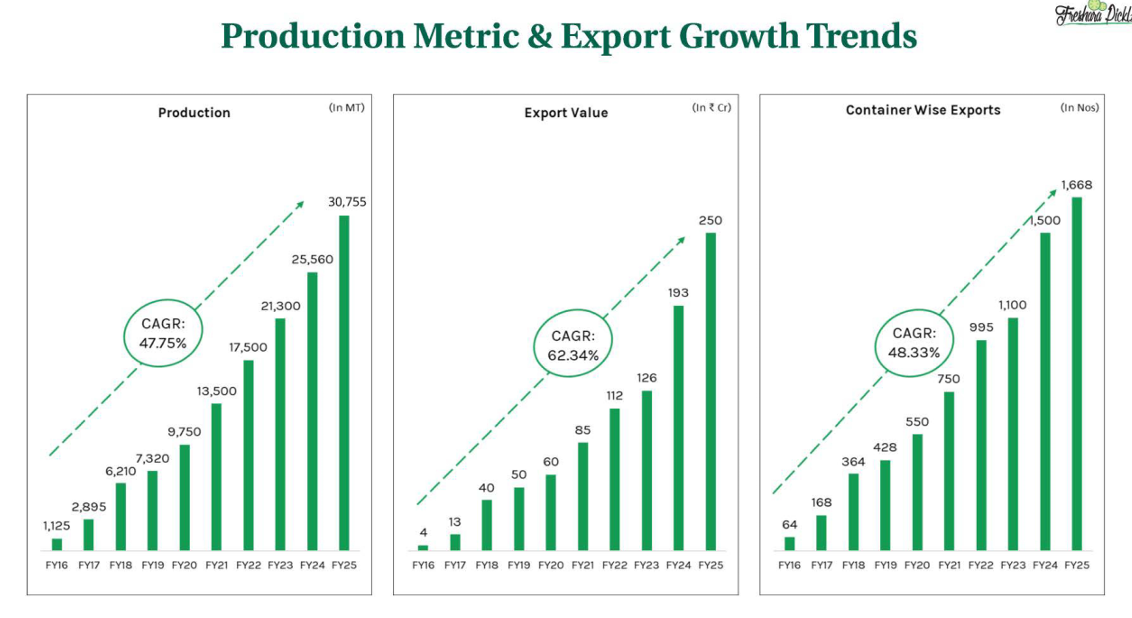

The India Advantage India has emerged as the world’s largest exporter of gherkins, commanding a ~20% global market share. The agronomic advantage is structural and distinct:

- Crop Cycles: Unlike Europe, Russia, or North America, where the climate allows for only one cucumber crop per year, the tropical climate of Southern India (specifically Karnataka and Tamil Nadu) supports two to three gherkin crops annually. This allows for year-round processing and better asset turnover.

- Labor Intensity: Gherkin harvesting is notoriously labor-intensive. The cucumbers must be hand-picked to avoid damage and to select the correct size grades (gherkins vs. larger cucumbers). India’s labor cost advantage is massive compared to Eastern Europe or Turkey, the traditional competitors.

- Contract Farming: The industry operates on a contract farming model. Freshara has empanelled over 4,000 farmers across 22 districts. This network acts as a high barrier to entry; a new competitor cannot simply build a factory—they must spend years building trust and logistics networks in rural hinterlands to secure raw material.

Investment Thesis & Valuation

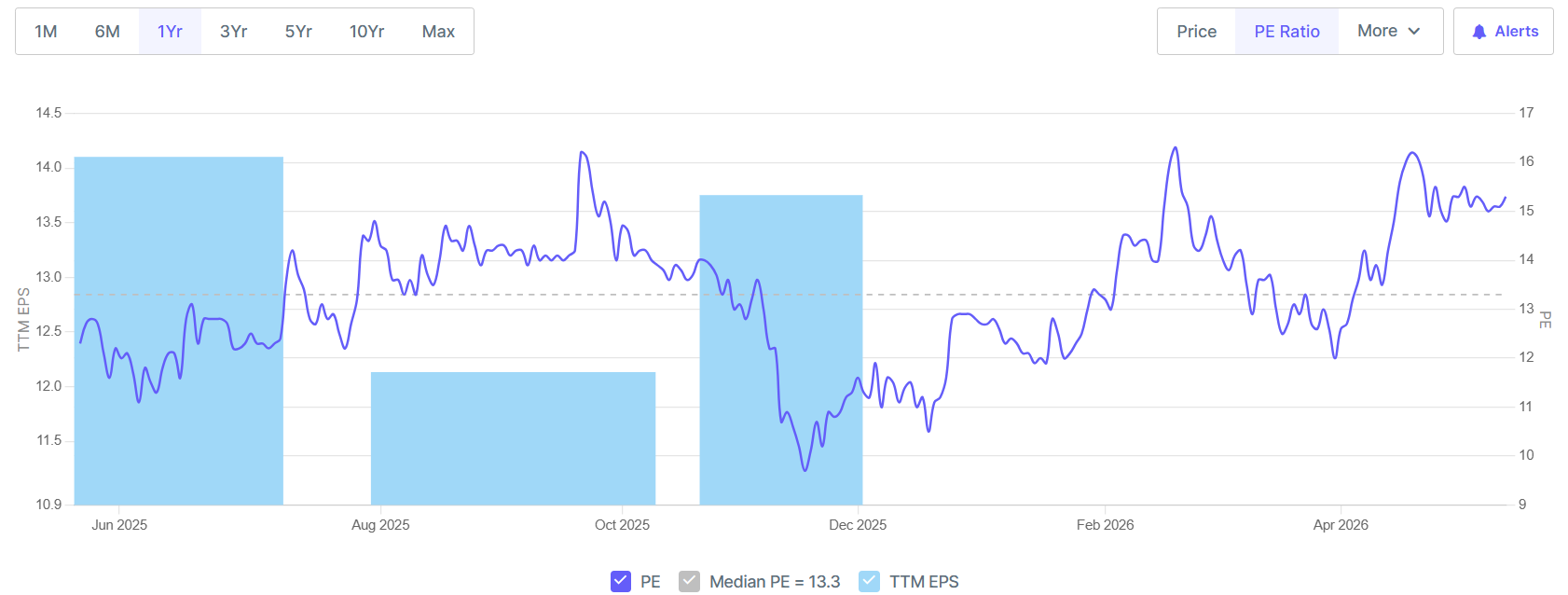

In the fragmented and often commoditized landscape of India’s Small and Medium Enterprise (SME) agri-processing sector, Freshara Agro Exports Limited (Freshara) has emerged as a singular anomaly. While the market continues to value the company as a traditional bulk exporter of gherkins—assigning it a modest trailing P/E of ~14.7x—our analysis indicates that Freshara is in the early stages of a fundamental metamorphosis. It is transitioning from a low-margin, volume-driven commodity trader into a vertically integrated, multinational food processing entity.

The investment thesis is predicated on a “Triple-Catalyst” convergence that has materialized in the first six weeks of 2026

- Strategic Alpha (The Spanish Acquisition): The acquisition of the distressed assets of Aceitunas Sarasa in Spain is the cornerstone of our bullish stance. By acquiring a historic European brand, established distribution channels, and high-quality production assets for a distressed valuation of ~€7.7 million (approx. ₹82.5 Cr), Freshara has effectively purchased a terminal in the high-value European retail market. This deal allows Freshara to capture the arbitrage between Indian manufacturing costs and European retail price points, transforming its margin profile.

- Macro Alpha (The US Trade Accord): The interim trade agreement between the United States and India, announced on February 2, 2026, serves as a massive tailwind. The reduction of retaliatory tariffs from 50% to 18% on Indian agricultural exports fundamentally alters the unit economics of shipping to North America. This policy shift neutralizes the competitive advantage previously held by Mexican and Turkish exporters, positioning India—and specifically Freshara—to reclaim dominance in the massive US fast-food and retail pickle market.

- Operational Alpha (Capacity & Product Mix): The operationalization of Unit II in Tirupattur, Tamil Nadu, doubles the company’s processing capacity to over 75- 100 Metric Tonnes Per Day (MTPD). More importantly, it enables a shift in product mix from bulk drums (industrial) to retail jars (consumer-facing) and high-margin innovations like Banderillas and marinated olives.

Synergy Map: The “Farm-to-Fork” Integration

The strategic logic of this deal is anchored in the cross-pollination between Indian low-cost production and European high-value consumption. We identify three distinct synergy vectors:

- Cost Rationalization (The “Reverse” Supply Chain): Freshara intends to shift the labor-intensive pre-processing stages—cleaning, grading, sorting, and initial brine fermentation—from the Spanish facilities to its Indian units in Tirupattur. India offers a significant labor cost arbitrage compared to Spain. These semi-processed goods will then be shipped to the Spanish facilities for final value addition (flavoring, marinating) and retail packaging. This hybrid model lowers the consolidated Cost of Goods Sold (COGS) while maintaining the “Product of Spain” or “Packaged in Spain” designation where applicable, which commands a premium.

- Product Portfolio Expansion (The Olive Entry): Aceitunas Sarasa brings deep, multi-generational expertise in Olives, a segment where Freshara had limited presence. The global olive market is significantly larger and more premium than the gherkin market. The combined entity will offer a comprehensive “Pickle & Olive” basket to global retailers, increasing stickiness with major European buyers like Carrefour, Mercadona, and Aldi. Freshara can now cross-sell Indian gherkins to Sarasa’s olive customers and Spanish olives to Freshara’s existing US/Russian clientele.

- Distribution Network Acceleration: Building a European retail distribution network from scratch typically takes 5-7 years of aggressive marketing and slotting fees. Through this acquisition, Freshara gains immediate access to Sarasa’s established distribution channels across Europe. This bypasses the gestation period and accelerates the revenue recognition cycle.

The US Trade Deal: A Tailwind for FY27

The global trade environment for gherkins has been volatile, dictated by protectionist tariffs and geopolitical alignments. In 2024 and 2025, Indian exporters faced severe headwinds from US tariffs, which escalated to nearly 50% on certain Harmonized System (HS) codes, rendering Indian gherkins less competitive against duty-free supplies from Mexico or lower-tariff goods from Turkey.

The February 2026 Turnaround The bilateral interim trade agreement between the US and India, effective immediately as of early February 2026, reduces these retaliatory tariffs to 18%. This reduction in the landed cost of Indian gherkins in the US serves two critical functions for Freshara:

- Volume Recovery: It re-opens the US market for bulk industrial supplies, particularly to fast-food chains (QSRs) that require massive volumes of sliced pickles for burgers. These buyers are price-sensitive; the 50% tariff had forced them to look elsewhere. The 18% rate brings India back into the competitive band.

- Margin Retention: Previously, to remain competitive in the US, Indian exporters had to absorb a significant portion of the tariff costs, compressing their FOB realization. The reduction allows Freshara to retain a higher portion of the FOB price, directly expanding gross margins.

Company Overview & Strategic Evolution

History and Milestones

Freshara’s journey reflects the maturation of the Indian agri-export sector. Incorporated in 2015 as a partnership firm (Freshara Picklz Exports), the company transitioned to a public limited entity in 2023 and listed on the NSE SME platform in October 2024.

- 2015-2019 (Foundation Phase): The company focused on establishing the basics—bulk gherkin exports in drums and building the farmer network. This phase was characterized by low margins but high volume growth.

- 2020-2023 (Diversification Phase): Diversification into Jalapeños, Baby Corn, and Chillies. Commissioning of Unit I retail lines allowed the company to start serving supermarkets directly.

- 2024 (Capital Market Entry): The IPO raised ~₹75 Cr, providing the war chest for the current expansion. By this time, Freshara had emerged as India’s 3rd largest gherkin exporter.

- 2025-2026 (Global Integration Phase): Aggressive inorganic growth (Spain acquisition) and capacity doubling (Unit II). This is the current phase, marked by a shift from “Exporter” to “Multinational Processor.”

Manufacturing Assets

Freshara operates two primary facilities in the Tirupattur District, Tamil Nadu. This location is strategic, situated in the heart of the gherkin-growing belt (Krishnagiri/Dharmapuri) and close to the Chennai port for export logistics.

- Unit I (Velakalnatham): The original processing facility. Over time, this unit has been optimized for specialized retail packing and smaller batch runs.

- Unit II (Chengilikuppam): The new growth engine.

- Capacity: 75-100 Metric Tonnes Per Day (MTPD).

- Automation: Equipped with advanced retail packing lines capable of producing 6,000 jars per hour, expandable to 18,000 jars per hour.

- Technology: Features automated grading, pasteurization, and vacuum packing systems that ensure consistency required by global food safety standards (BRCGS, IFS).

The Farmer Network: The Unseen Moat

Freshara does not own land; it owns relationships. The company works with 4,000+ marginal farmers across Tamil Nadu, Karnataka, and Andhra Pradesh.

- The Contract Model: Freshara supplies seeds and technical inputs to the farmers. This ensures two things:

- Quality Control: By controlling the seed, Freshara controls the variety and quality of the output.

- Traceability: This allows Freshara to trace every jar back to the specific farm, a mandatory requirement for FDA and EU compliance.

- Asset-Light: This model reduces capital intensity while securing the supply chain against spot market volatility.

Recent Performance (H1 FY26 & Q3 FY26 Trends)

H1 FY26 (Apr-Sep 2025) Snapshot:

The company reported a defining period of growth:

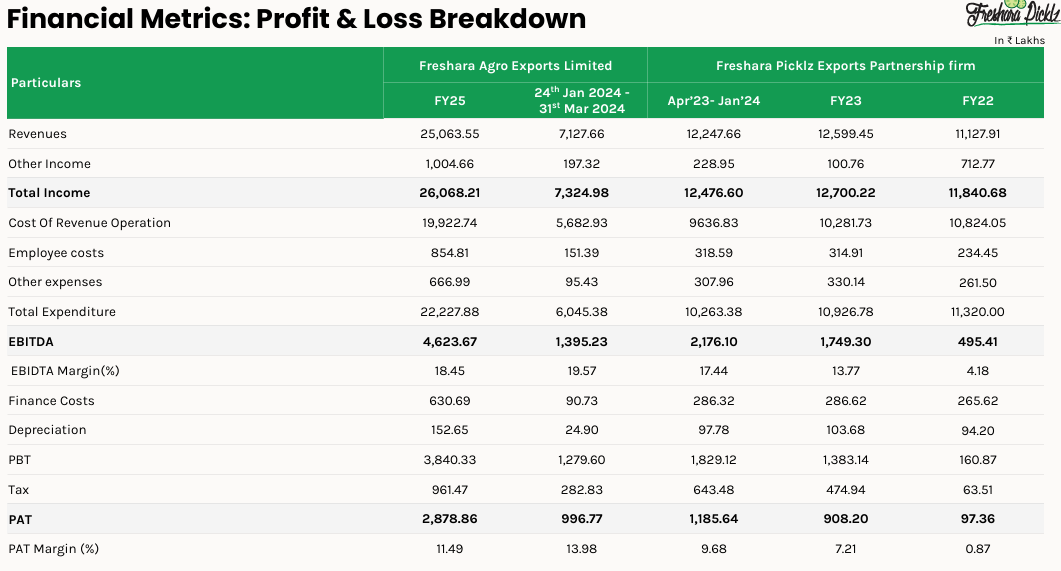

- Revenue: ₹140.9 Cr (+31% YoY).

- EBITDA: ₹24.4 Cr (+30% YoY).

- PAT: ₹14.9 Cr (+31% YoY).

- Margins: EBITDA Margin remained stable at ~18.1%; PAT Margin at ~11.1%.

Balance Sheet Strength

- Debt Profile: As of FY25, Freshara had a Debt-to-Equity ratio of ~0.74, which is healthy for a capital-intensive processing business. The acquisition is funded via a mix of internal accruals, warrants (equity), and moderate debt, ensuring the balance sheet remains leveraged but not stressed.

- Working Capital: The business is working capital intensive (Receivables ~90 days). However, debtor days improved significantly from 259 days in previous years to 122 days in FY25, indicating better collection efficiency.

- Return Ratios: ROCE stands at 24.8% and ROE at 36.9%. These are “Best-in-Class” numbers, superior to many larger FMCG players, indicating efficient capital deployment.