Over the last month, our inbox and phone have been full of the same two questions from investors: “Should I stop my SIPs?” and “Should I sell now and buy back when markets bottom out?” Both questions come from the same place – fear. And both lead to the same destination — permanent loss of wealth.

Maximum wealth is destroyed not by the market crash itself, but by how people react to that crash.

The Two Mistakes Destroying Wealth Right Now

Mistake #1 – “I’m stopping my SIPs because of the war”

One investor told us he was stopping all his SIPs because he expects the Iran-US conflict to be followed by a China-Taiwan war, a Russia-Ukraine flare-up, and a prolonged global slowdown.

Here’s the problem with that logic. Wars have happened before. Pandemics have happened before. Great crashes have happened before. Even investors who put money in just before the 50% fall of 2008 – the worst possible timing – still earned roughly 11–12% annualised over the following ten years, provided they stayed invested.

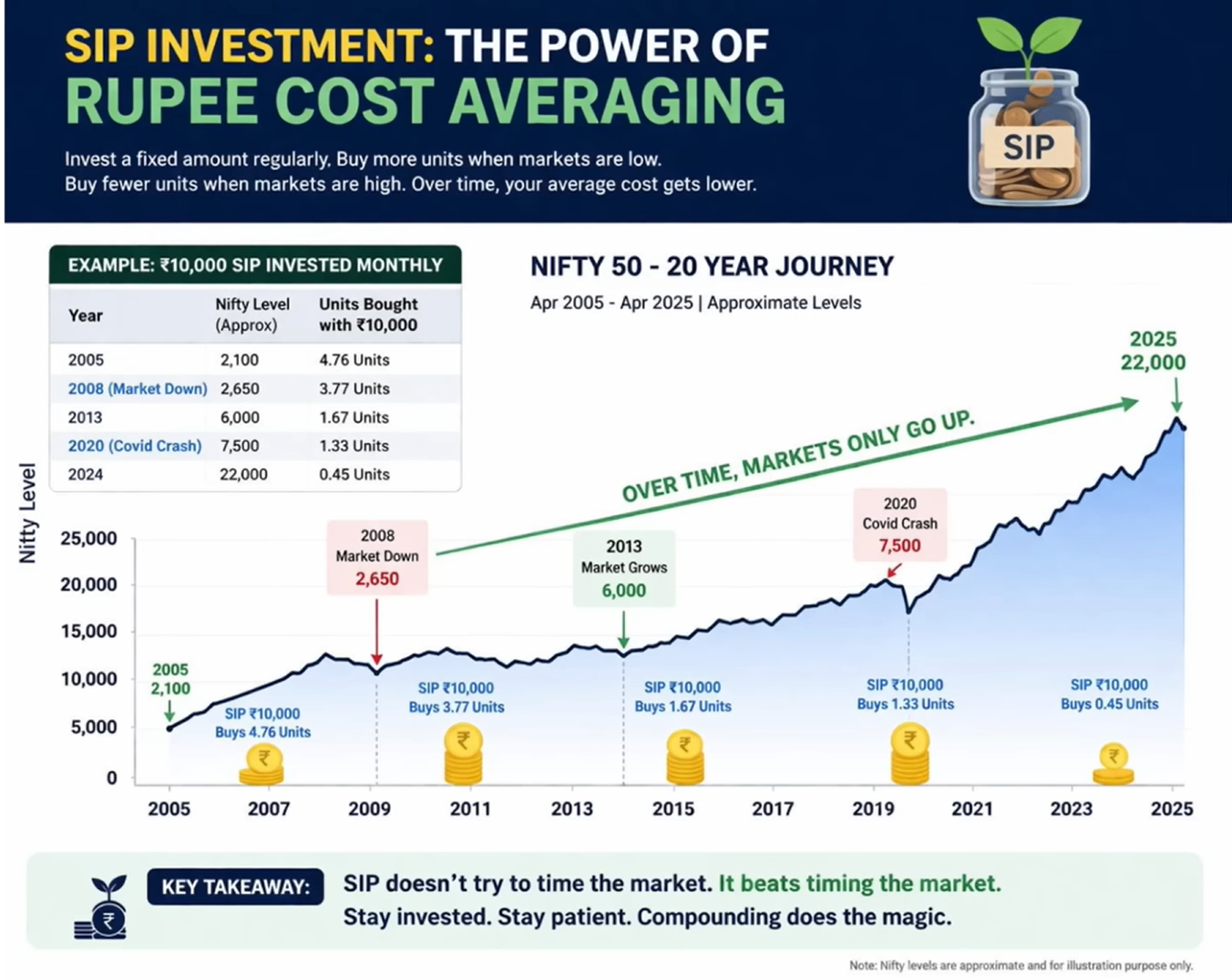

And stopping SIPs when markets fall is the exact opposite of how SIPs create wealth. You’ve been happily buying units at higher prices for months – and now that the market is offering you the same assets at lower prices, you want to stop buying? That defeats the entire purpose of rupee cost averaging.

In fact, if you genuinely believed a prolonged slowdown was coming, the internally consistent move would be the reverse: book profits on your lump-sum holdings, park the money safely, and increase your SIP amounts so you accumulate more units through the downturn. Stopping SIPs while staying fully invested in your old units isn’t a strategy – it’s panic wearing the costume of a strategy.

Mistake #2 – “I’ll sell to protect my capital and buy back at the bottom”

This is the classic. It sounds prudent. It never works.

Markets fall sharply – and they bounce back equally sharply. In just one recent week, the market rose about 6.5%, with a single Wednesday delivering a gain of nearly 3.8%. If you had sold during the fall, hoping to re-enter at “the bottom,” you would have watched that entire recovery from the sidelines.

In all our years of doing this, We have not seen a single investor who sold into a falling market and successfully bought back at the bottom. Not one. What actually happens is worse than just missing the rebound: you pay capital gains tax on the units you sold, and then you buy back the same units at a price higher than where you sold them. You lose twice.

The Statistic That Should End This Debate

This has been back-tested across 1-year, 5-year, 10-year and 20-year timeframes, over a thousand times:

If a market or fund delivers 12% a year, and you miss just the 10 best days, your return collapses from 12% to roughly 6%. And five or six of those ten best days almost always occur right after a crash.

The best days and the worst days live next door to each other. You cannot avoid one without missing the other. This is why the people who sell into a crash reliably underperform the people who simply do nothing.

What we are Buying – and Why

If you’re not willing to buy stocks and equity funds at these levels, We honestly don’t know what you were waiting for. Here is exactly what we’ve added, with the reasoning behind each position:

| Position | Type | The One-Line Thesis |

| TCS | Large-cap IT | AI is a tailwind, not a threat — order book tells the real story |

| Indraprastha Gas (IGL) | City gas distribution | Closest to the customer = best margins; temporary LNG pain |

| Windlas Biotech | Pharma CDMO | Discussed previously; thesis intact |

| ITC | FMCG / dividend | Bought purely for the ~5% dividend yield |

| Axis Value Fund | Mutual fund | Like the allocation and the value discipline |

Technology: The Narrative vs. The Ground Reality

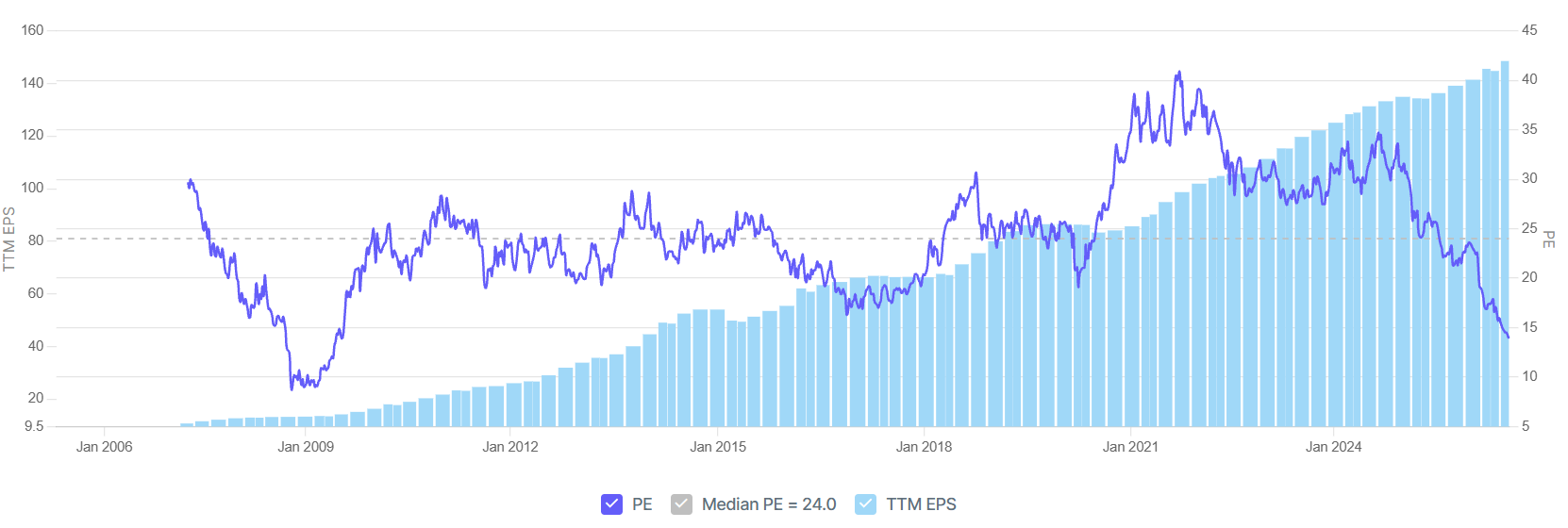

The loudest story in the market right now is that AI will kill legacy Indian IT companies. The ground reality is the opposite. Look at TCS: five to six large deal wins in the last three months alone – the UK’s national health insurance programme, Danish insurer Tryg, BSNL in India – and a striking number of these fresh orders are specifically for AI transformation work. The order book stands at around $9 billion.

TCS Long Term MEDIAN VS CURRENT PE

Meanwhile, the stock trades at roughly 14 times earnings – about as cheap as I can remember it ever being. When the narrative says “disruption” and the order book says “AI is our growth engine,” I side with the order book. This is a classic case of confusing the story with the evidence.

Indraprastha Gas:

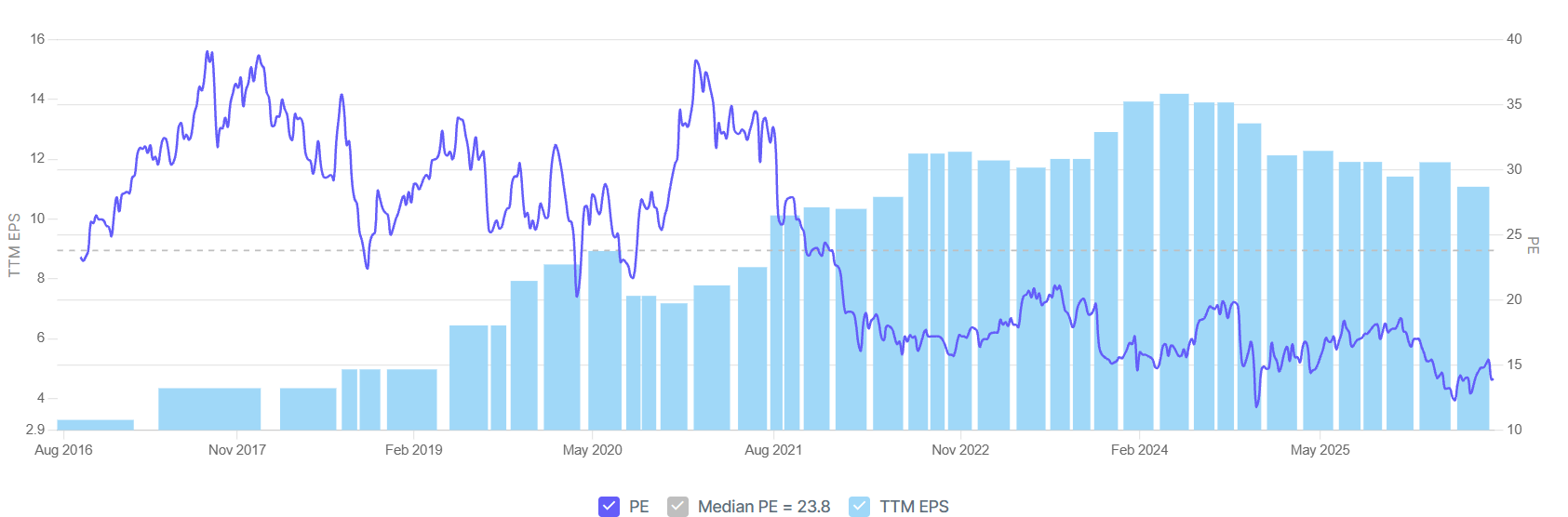

Our framework for the oil and gas value chain is simple: the closer a company sits to the end customer, the better its margins. City gas distributors sit right at the end of that pipeline.

IGL Long-Term MEDIAN VS CURRENT PE

IGL has fallen sharply because of a bottleneck in LNG supply – much of India’s LNG comes from the Middle East, mainly Qatar, and disruption around the Strait of Hormuz has pushed up input costs. IGL can’t raise prices aggressively even as the gas it buys gets costlier, so margins are squeezed. But this is a temporary supply-chain problem pressing down on a structurally well-positioned business. That combination – good business, temporary problem, fallen price – is precisely what we want to buy.

ITC: When a Blue Chip Pays You 5% to Wait

ITC is now available at a level where its dividend yield alone is around 5%. We are not buying it for a re-rating story or a growth story – We are buying it purely for that yield. At 5%, you’re being paid bond-like income to hold a durable consumer franchise. Everything else is optionality on top.

Why We Are Bullish on India Over the Next 12-18 Months

Here’s a pattern We’ve watched play out repeatedly over 20 years: when markets fall, negativity seeps into everything. Suddenly the commentary becomes “India’s fundamentals are bad, we don’t make anything, we have no oil, no rare earths, we depend on everyone.” Let the Nifty hit 30,000, and the same voices will rediscover our IT sector, our pharma sector, and everything else we have going for us. Price action drives the narrative – not the other way around.

Strip out the noise and look at what’s actually true:

- Growth: India remains one of the fastest-growing large economies, running at 6–7%.

- Inflation: Largely under control, especially compared with our peers.

- Fiscal discipline: Actually improving, not deteriorating.

- China+1: The manufacturing and supply-chain shift continues to work in India’s favour.

- Earnings: Banks, capital goods and infrastructure are set to grow earnings 12–14%. Watch the next two to four quarters — the numbers will do the talking

The Nifty trades roughly in line with its 10–15 year averages. Neither cheap nor expensive — which, combined with growing earnings, is a perfectly fine starting point.

The One Genuine Bottleneck: FII Selling

The only real headwind we see is foreign institutional selling. And I don’t believe FIIs are selling because they doubt India’s growth. They’re selling because the maths of investing here has gotten harder: if a foreign investor must pay 12.5% capital gains tax on profits in India, then India has to outperform competing markets by that margin just to break even for them. Add a strengthening US dollar against the rupee, and the hurdle gets higher still.

Our view: the government should seriously consider cutting these taxes for foreign investors – it would attract capital and help stem the rupee’s fall in one move. We don’t buy the argument that a weaker rupee is fine because it makes exports competitive. If the tax treatment improves while the dollar remains this strong, We wouldn’t rule out a flood of foreign capital into India. Maybe not immediately – but at some point, we think it’s likely.

The Five Takeaways

- The crash doesn’t destroy wealth – your reaction to it does. Doing nothing is usually the winning move.

- Never stop SIPs in a falling market. Lower prices are the whole point of rupee cost averaging.

- Nobody catches the bottom. Selling to “buy back lower” means paying taxes and repurchasing higher – losing twice.

- Miss the 10 best days and your returns halve – and most of those days come right after crashes.