Have we seen this pattern before?

A mission-critical infrastructure product, multi-decade switching costs, heavy upfront R&D that suppresses today’s margin, then operating leverage as the installed base compounds. The same playbook is being played out across CDMO and Precision Engineering domain

At roughly ₹10,500cr market cap and ~30x trailing earnings, the market is paying ~30x for a business growing the top line designed to grow at 20% with a 25%+ earnings runway as the investment phase matures – a PEG near 1. It is fair-to-attractive if you believe the expensed R&D becomes tomorrow’s margin. The stock falling 31% while the business grew 23% means the expectations baked into the price have dropped, not the fundamentals. That divergence is the entire thesis.

The convex case

- Sector-wide de-rating drags a product firm down with the service shops – wrong basket.

- Purple Fabric is a cheap option on AI adoption, not AI disruption.

- Mainframe-to-cloud migration is a years-long, sticky tailwind.

- Operating leverage + AMC compounding can lift margins materially.

The market is selling “Indian IT.” It is accidentally selling a research-led product company on the same theme.

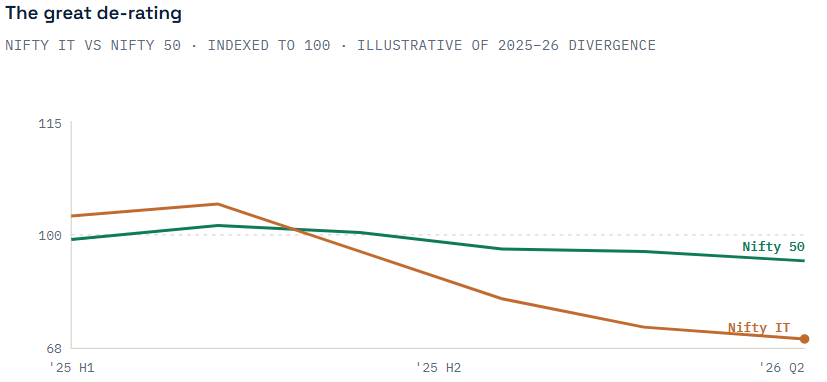

Indian IT sector drags on a single story

“India is falling behind in the AI era.” The selling has been indiscriminate. And indiscriminate selling is where mispricings live – because the index treats a labour-arbitrage service firm and a research-led product firm as the same. They are not.

For most of two decades, Indian IT was the market’s darling. In 2026 it became its punching bag – one of the worst-performing sectors of the year, hitting a 30-month low and underperforming the Nifty 50 by roughly 32% over a five-month stretch.

The reasons being debated across the financial press are real, if not yet proven: fear that AI can write code and compress billing, weak US discretionary tech budgets, Accenture trimming guidance, and the heaviest foreign-investor selling in over 15 years. The sector’s weight in the Nifty 500 has collapsed to about 5.5% – its lowest in a decade against a long-run median near 10.5%

Earnings kept rising; it was the multiple that fell – record profits, compressed valuations. So far the evidence points to a sentiment de-rating, not an earnings collapse.

Pavlovian Association

The current sell-off reflects a classic association bias: investors have come to associate “Indian IT” with labour-arbitrage services, causing research-led product companies such as Intellect to be marked down alongside service peers despite materially different business models.

Here is the trap the index sets. A sector ETF can’t tell the difference between a company that sells hours and a company that sells intellectual property. When the tide goes out on “Indian IT,” both get marked down together. Intellect is the second kind – and that confusion is the opportunity.

The Divergence- One percent

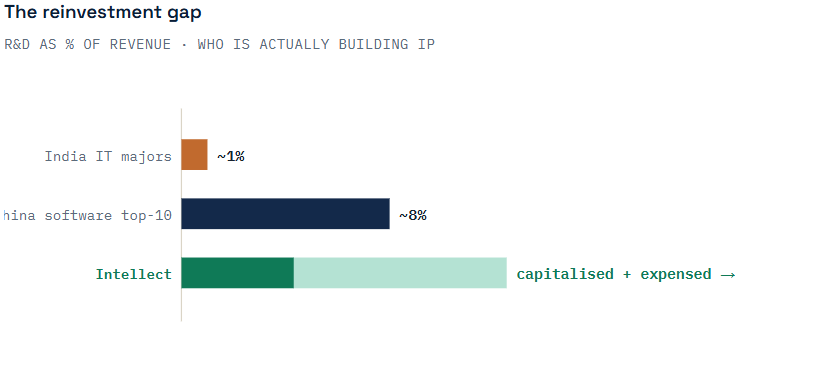

Here is the fact that reframes everything. India’s top ten software companies invest roughly 1% of revenue in R&D. China’s top ten invest over 8%. The Indian giants have returned about three-quarters of their cash profits to shareholders as dividends and buybacks, reinvesting barely a tenth back into the business.

That is the labour-arbitrage model: rent out engineers, bill by the hour, harvest the cash. It worked beautifully for twenty years. The market’s fear is that AI quietly dismantles it.

Sources: India ~1% & China >8% per industry commentary (Urbanomics, 2025). Intellect’s solid bar ~ the product-development it capitalises (~4% of revenue); the faded extension is the far larger slice expensed straight to the P&L.

Intellect runs the opposite playbook. Roughly one in five of its ~6,300 people sit in pure research. It pours about 2 million engineering hours a year into R&D — 16 million over the last eight years — and filed close to 100 patents last year alone. It began investing in cloud and AI back in 2017, three to four years ahead of the wave, because in a product business you must build for the next cycle before it arrives.

Margins now, or the moat forever

This is the part that frustrates investors – and the part worth understanding. When Intellect spends on R&D, most of it is expensed immediately. It hits the profit line today, even though the payoff arrives years later. So reported margins look soft precisely because the company is investing in tomorrow.

The result is a recurring standoff. Analysts want a clean 25%+ margin this quarter. Management deliberately ploughs ~5% of margin back into the next platform, accepting lower profits today to extend what Michael Mauboussin calls the Competitive Advantage Period — the number of years a business can earn returns above its cost of capital. Short horizon versus long horizon, fighting over the same rupee.

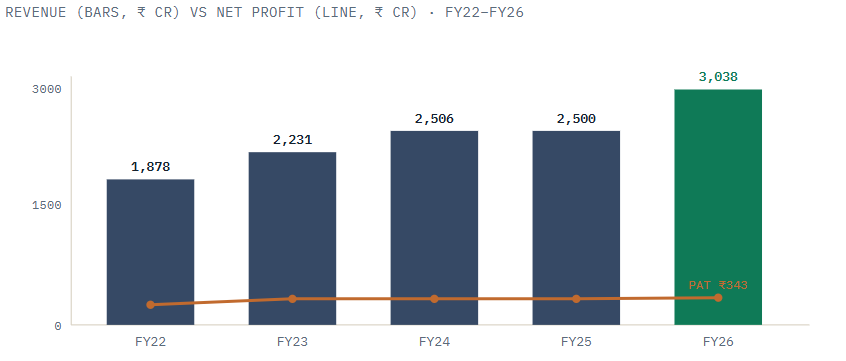

Revenue climbs; profit waits

Revenue compounded steadily for Intellect while net profit stayed almost flat from FY24-FY26 (~₹334cr → ₹343cr). That gap is the R&D bill – value being built off the income statement, not destroyed. FY25’s flat top line was largely deal-timing, not decay. Figures per company filings / ICICIdirect.

“Instant gratification” investors see flat profits and leave. The patient ones ask a different question: what is being built with the money that isn’t showing up as profit yet?

From product, to platform, to AI – The 80% That Matters

Strip away the product complexity and Intellect’s business model is simple: it provides the mission-critical software that powers banks and insurers across core banking, lending, payments, treasury, trade finance, wealth management, and insurance. These platforms typically remain embedded for +10 years, as replacing them involves significant operational, regulatory, and execution risk.

The resulting high switching costs drive durable customer relationships, strong revenue visibility, and an annuity-like stream of recurring revenue.

The pivot – two platforms, one bet

The company has shifted from selling products to selling platforms, and platform revenue grew 141% in FY26. Two assets carry the optionality:

eMACH.ai – an open-finance platform that breaks banking into 329 microservices, 535 events and 1,757 APIs. Its killer use case is Mainframe-to-Cloud: helping legacy banks escape 1970s infrastructure without a big-bang rewrite. That migration is a multi-year, industry-wide tailwind.

Purple Fabric – the genuine call option. An enterprise AI platform aimed at measurable business impact, not chatbot theatre: AI that reads insurance submissions, runs governance and compliance, and makes decisions with traceability regulators accept. Marquee US and Canadian financial institutions are already live. If the market fears AI eats Indian IT, Purple Fabric is Intellect selling the picks and shovels instead of gold.

The customer mix is migrating up-market toward Tier-1 global banks, and the developed-economy share keeps rising. Product risk reduced through R&D, market risk through geography, customer risk through deep, long relationships. That is the whole design.

A balance sheet that lets it wait

A company can only afford to depress its own margins for years if it isn’t fighting for survival. Intellect isn’t. It carries roughly ₹1,000cr+ of cash, effectively no debt, and converts profit into real cash – operating cash flow actually runs ahead of reported earnings. That fortress is what funds the patience.

| Metric | Value | |

|---|---|---|

| Total income | ₹3,161 cr | +23% YoY |

| License-linked rev | ₹1,667 cr | +34% YoY |

| EBITDA | >₹700 cr | 19.1% margin |

| Net profit | ₹343 cr | ~flat |

| Net cash | ~₹1,257 cr | Debt-free |

| ROCE / ROE | 16.8% / 13% | depressed by R&D |

| Promoter holding | 29.7% | – |

Those returns ratios look ordinary – but they are artificially low, dragged down by a growing cash pile and front-loaded investment. Management’s stated ambition is ~20-25% EBITDA margins as platforms scale and AMC compounds margins can expand.

One Response

As always great insight from you sir. You have already spoken about this company in your video and again here regularly validates even more strongly. Thanks sir