The biggest mistake we made in our 20s was not buying the wrong stocks. It was misunderstanding what money was supposed to do.

Back then, we thought markets existed to make us rich. We never saw them as a place where wealth gets multiplied slowly, patiently, over decades. So we chased the wrong things – futures, options, quick trades – and burnt our fingers fairly quickly. If you are a retail investor trading options or futures, you are always just two leaps ahead of the wolf. Sooner or later, it catches up.

But here is the deeper realisation, and it took us a while to see it – even if we had succeeded at what we were trying to do back then, it would not have changed our life. Suppose you find a multibagger with one or two lakhs and it doubles. Great. Four lakhs. Your life is exactly the same.

After doing financial consulting for hundreds of people across age groups – and after living through these stages ourselves – we have come to a simple conclusion. Most people are doing their financial planning completely wrong. Not because they pick bad funds or bad stocks, but because they ask the wrong question.

People keep asking “where should I invest?” The question itself is wrong. The right question is – what stage of life am I in? Your financial decisions should be built on your stage of life, not on what the market is doing this month.

So here is the framework, decade by decade.

Your 20s – Build the Habit, Forget the Returns

In your 20s, your job is not to earn returns. Your job is to build the habit of saving.

That sounds boring, we know. But it is the single most useful thing you can do at this age. If you are saving any money at all, what matters is consistency – month on month, without fail. Even if it is 100 rupees, 500 rupees or 1,000 rupees. The amount is almost irrelevant. What you are really building is the muscle – the quiet confidence that says, yes, I know how to save.

Do not obsess over how much that saving is growing. It will not grow to anything meaningful at this stage anyway, and that is fine. The corpus is small – the habit is the asset.

A quick caveat – this is not for everyone. If you are the 21-year-old child of an industrialist, you can probably holiday in Europe already. This is for most people – those who start lower middle class or middle class, or even those who are well-off but want to build their own base of assets and then enjoy it.

For everyone in that boat, take it from someone who is 46, and from a lot of others who will tell you the same thing:

- Focus on forming the habit of investing month on month

- Do your SIPs, invest in mutual funds

- There is no harm taking some risk with some part of your capital – but never all the risk with all of your capital

Chasing multibaggers with two lakhs and doing options trading on the side is not investing. It is just an expensive way to learn this lesson later.

30 to 45 – The Formative Years, When Compounding Wakes Up

These are the years when things start to change – quietly at first, then unmistakably.

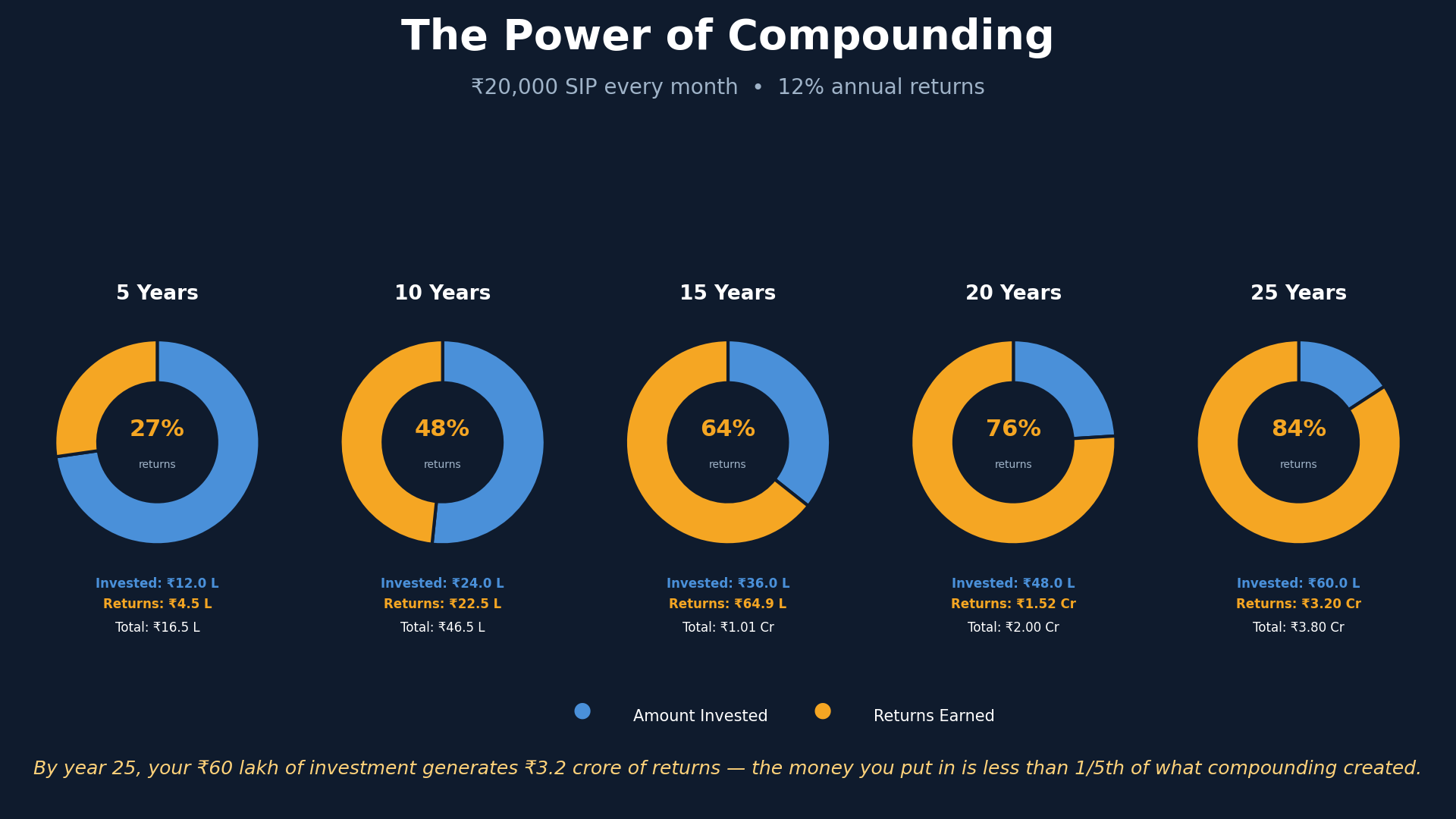

Somewhere in this window, your corpus crosses a size where wealth starts to grow on its own. In our experience, the number where wealth really begins to explode is around 1 crore. We do not fully know why that threshold feels so real, but it does. Think about the simple math – at 50 lakhs growing at 10%, your money adds 5 lakhs a year by itself. At 1 crore growing at 10 to 12%, roughly 12 lakhs gets added every year without you lifting a finger – if the job is being done right.

This is also when the penny drops. You look back and realise how pointless it was to chase multibagger returns with two or three lakhs, or to gamble on options and futures. The real driver of your wealth was never a clever trade. It was your income, your savings rate, and time.

So what should you actually do in these years?

- Focus primarily on your job and your career – that is your biggest compounding engine right now

- Keep the SIPs and mutual fund investments running like clockwork

- Buying a small property and paying EMIs over time works too, if that suits you – the point is to keep creating assets

- Avoid an inflationary lifestyle

That last point deserves a pause. Instead of two Europe or America vacations every three years, make it one. Not because vacations are bad, but because you have a long life ahead of you – and every inflationary expense you cut today lets you enjoy life in a far more meaningful way later.

One more thing. The day you start using the word compounding about your own investments – and it is genuinely happening on its own, money getting invested automatically, growing without your daily attention – that is the day you know you are already on the way to creating serious wealth.

45 to 60 – Money as Protection, and the Art of Not Blowing It Up

This is the bracket we are in ourselves, at 46. And having consulted for a lot of people in this age group, we can tell you the most important rule of this phase in four words – avoid the costly mistakes.

If the earlier decades were done right, you have reached a place where working is now a choice. For us personally, it is – we do not have to work for money anymore. Some people in this bracket still need to work, some are just getting started, some could retire tomorrow. But broadly, if things have gone reasonably well, you are in a safe position to live a normal, peaceful life without chasing excess growth.

And yet – here is the strange thing we have observed. This is precisely the age when people want to experiment the most. They do not want to think about protection. They want to get aggressive. They want to take the risks they never took. And this is exactly where we have seen people make the biggest financial mistakes of their lives.

There is another lesson from consulting people in this bracket. We have learned not to go by what people tell us about their money. We go by what we can sense about them.

Someone might say – I do not need this money for 5 to 7 years, invest it aggressively. But talking to him, you can sense he is the kind who loves to go out, party, mingle with the big shots – he may have a crore coming in next month and nothing left to invest the month after. Another person – a lawyer, a chartered accountant, a doctor, an IT professional – has a steady salary growing 8 to 10% a year, and you can sense his life will go exactly as predicted. To him, you can comfortably say – go ahead, take that home loan, and keep investing in funds alongside.

People reveal who they are in how they talk about money, far more than in what they claim about it.

So our biggest advice for this bracket:

- Think of money as protection – as the backbone that supports you

- Do the boring things – emergency planning, insurance

- A small slice in risky ventures or the occasional fancy gadget or car is fine – you will do it anyway

- But above all, avoid the huge mistakes – one big blow-up here can undo twenty years of quiet compounding

Your 60s – People Use Money Backwards

Most of the financial consulting we have done in recent years has been for people between 60 and 70. And one pattern shows up again and again – people use money backwards.

They do not do the things they dreamed of in their 20s, now that they finally can. Maybe the energy and will have faded. Maybe they are already busy planning inheritance and passing wealth to the kids. Whatever the reason, we see the same picture over and over – large sums parked in fixed deposits, benign old government securities, ultra-safe instruments, and real estate they do not even need. Sometimes not even rented out.

Here is the irony. This is actually the stage when you can afford to take risk with your capital. You could invest in startups. You could back younger people building new businesses. Think about it – losing 20 lakhs out of a 10 or 15 crore portfolio does not harm you at all. You are already wealthy enough to sustain the rest of your life.

And on inheritance – do not over-plan it. Everyone today already knows they have to make their own money as they grow older. It is not your job to pre-fund everyone’s future at the cost of your own present.

So if you are in this bracket – go travel the world. Do the things you wanted to do in your 20s. Take some risk. Enjoy your wealth. That is what it was for.

Pulling It All Together

Here is the whole framework in one place:

- In your 20s – form the habit of investing. Consistency over returns. SIPs over speculation.

- In your 30s and early 40s – focus on your career, build a system where money invests itself, keep lifestyle inflation in check, and let the corpus cross the threshold where compounding becomes visible.

- From 45 to 60 – treat money as protection. Insurance, emergency planning, and above all, no costly mistakes.

- In your 60s – stop using money backwards. Spend it, enjoy it, take the risks you can now easily afford.

And if you are an older person with kids – do not teach them how to pick stocks. Teach them the habit of saving. That is the real inheritance.

When people ask us where to invest, we know the question itself is wrong. It is never about where to invest. It is about what stage of life you are in – and letting that, not the market, drive your financial decisions.